Crystal Intelligence hosted this webinar with Clear Junction, a global leader in cross-border payments for regulated financial institutions, and CMS Law, a future-facing legal advisory service. The panel discussed the status of the UK crypto regulation regime and how recent developments could impact it, how the regulatory framework compares to those of the EU and US, and what this means for regulators, compliance professionals, exchanges, and investors.

The panel of experts included:

- Dima Kats, CEO of Clear Junction, who led the discussion.

- Marina Khaustova: COO of Crystal Intelligence.

- Sam Robinson: Partner at CMS UK.

- Clair Wermers: Partner at CMS Amsterdam.

Several polls were also shared with the two hundred-strong audience, with the results shared below. So, let’s dive in.

UK crypto regulation: The future is here

The webinar started with Clear Junction CEO Dima Katz remarking on its timing. It was held just hours after the Chancellor of the Exchequer, Rachel Reeves, announced the UK Draft Bill on crypto assets at the UK Fintech Week on April 29, 2025.

The proposed laws will bring crypto assets into the UK’s current financial regulatory fold, with implementation expected by the end of 2025. Katz was excited at the industry’s development, particularly surrounding stablecoins, but cautioned that a strong compliance regime must govern it.

What the proposed legislation means for UK crypto regulation and exchanges

Sam Robinson provided an overview of the current UK crypto regulatory landscape, mentioning the crypto AML regime (2020) and the crypto financial promotion regime (2023). He then discussed the newly announced UK crypto regulation regime, emphasizing the draft legislation just published that sets out the activities that will be regulated. The new regime aims to bring crypto assets within the existing framework for financial services, effectively performing the function of the EU’s MiCAR, with differences.

He then explained that the FCA will have a one-year application window for firms to apply to the new regime, including existing firms under the AML framework and new firms, although the backdate is not yet set.

Meanwhile, firms targeting UK customers from overseas must currently apply for a UK license, with some exceptions for institutional business through intermediaries. The proposed legislation will allow foreign entities to work through intermediary firms in the UK, reducing red tape.

He added that the Draft Bill included definitions of what will qualify as cryptocurrencies and what will constitute stablecoins, which should contribute to the growth of the UK crypto industry.

The poll below asked the audience how well-prepared they were for the new UK crypto rules:

Just 9% were fully prepared, although 60% were engaged in planning or assessment.

The incoming UK crypto regulatory framework and the EU’s MiCAR rollout

Clair Wermers provided insights into the EU’s MiCAR, noting that it already applies in the economic region, and licenses are currently being granted throughout the jurisdiction. She cited the example of the Netherlands, where it has been possible to apply for a license to trade since April 2024. She highlighted the importance of having a knowledgeable and active regulator.

Clair touched on the challenges the EU experienced when implementing the regime, noting that it was the culmination of a process that took seven years to complete. The first financial action plan was introduced in 2018, with MiCAR eventually coming into effect at the end of 2024.

She expressed optimism that, should the UK regime align itself with the EU framework, it would be easier to operate across the two jurisdictions as the process becomes more streamlined and efficient.

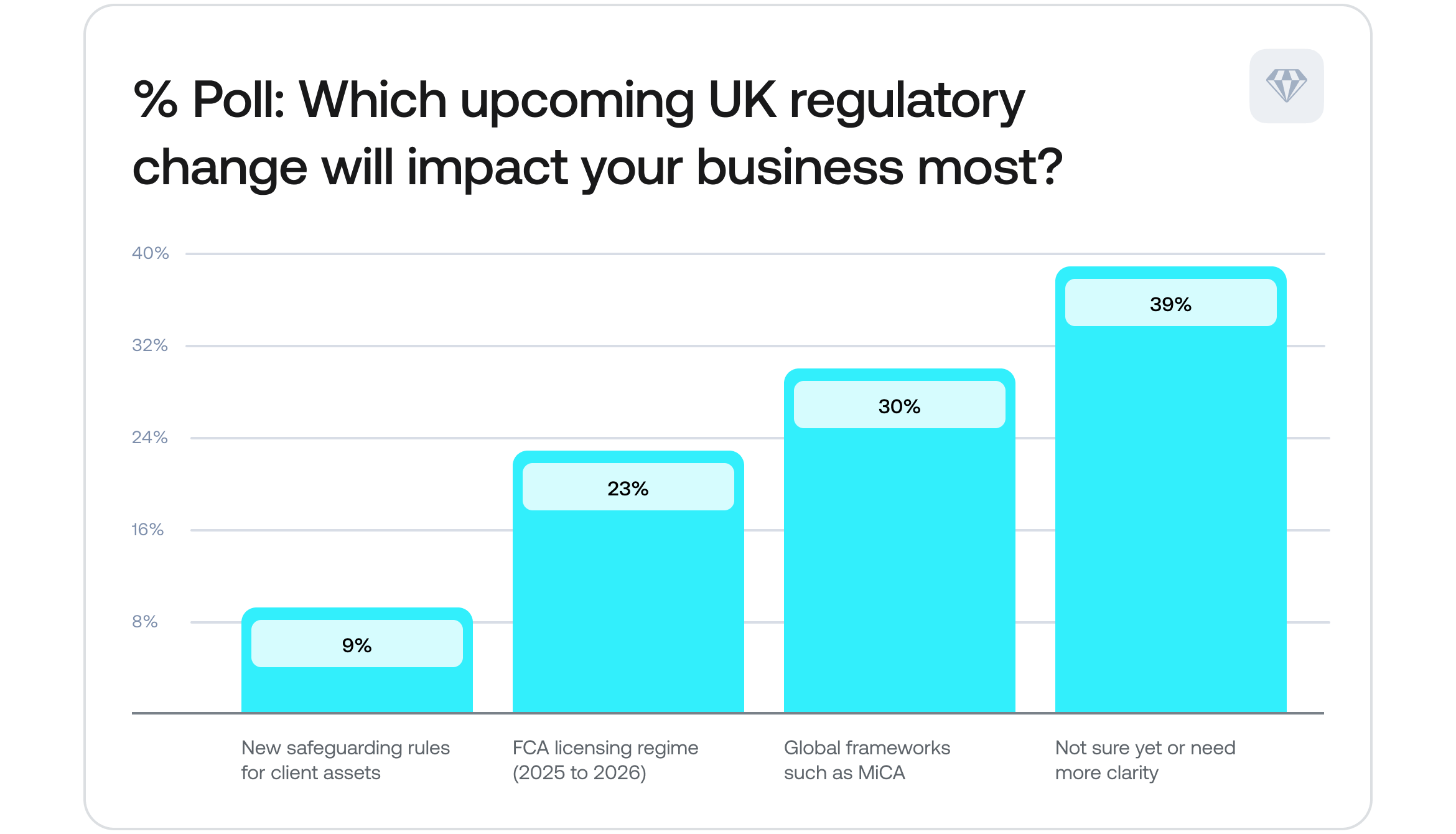

The poll below asked the audience which change to UK regulations would impact them the most:

A full 39% of respondents were unsure or needed more information.

The US crypto regulatory framework compared to the UK Draft Bill & the EU’s MiCAR

Marina Khaustova then spoke about the US crypto regulation approach, which Dima Katz likened to the “Wild West”. She highlighted that, as an entrepreneur, she shut down a crypto business that she had started in the US in 2018 at the beginning of the crypto winter. The stifling crypto regulatory environment made running a compliant business too challenging, and she opted to expand into Europe and then globally.

Marina noted that US federal oversight is becoming more streamlined and cohesive under the Trump administration. One example is that banks no longer need federal regulatory approval to engage in crypto activities. She also cited the incoming GENIUS Act to regulate stablecoins, which parallels the UK draft legislation’s focus on them.

Although these federal developments might codify crypto governance nationally, the US remains fragmented at the state level in the wake of rapid deregulation. While some states, such as Wyoming, embrace the status quo, encouraging developers of new technologies and innovation drivers, others move towards more established businesses, such as banks and other financial institutions, which are adopting digital asset trading.

The challenge the states face is how the industry polices itself at the state level. The inconsistencies between states, or regulatory arbitrage, create gaps into which scammers pour, and Ponzi schemes have been detected. Consequently, training law enforcement to decipher the babble and respond successfully is challenging.

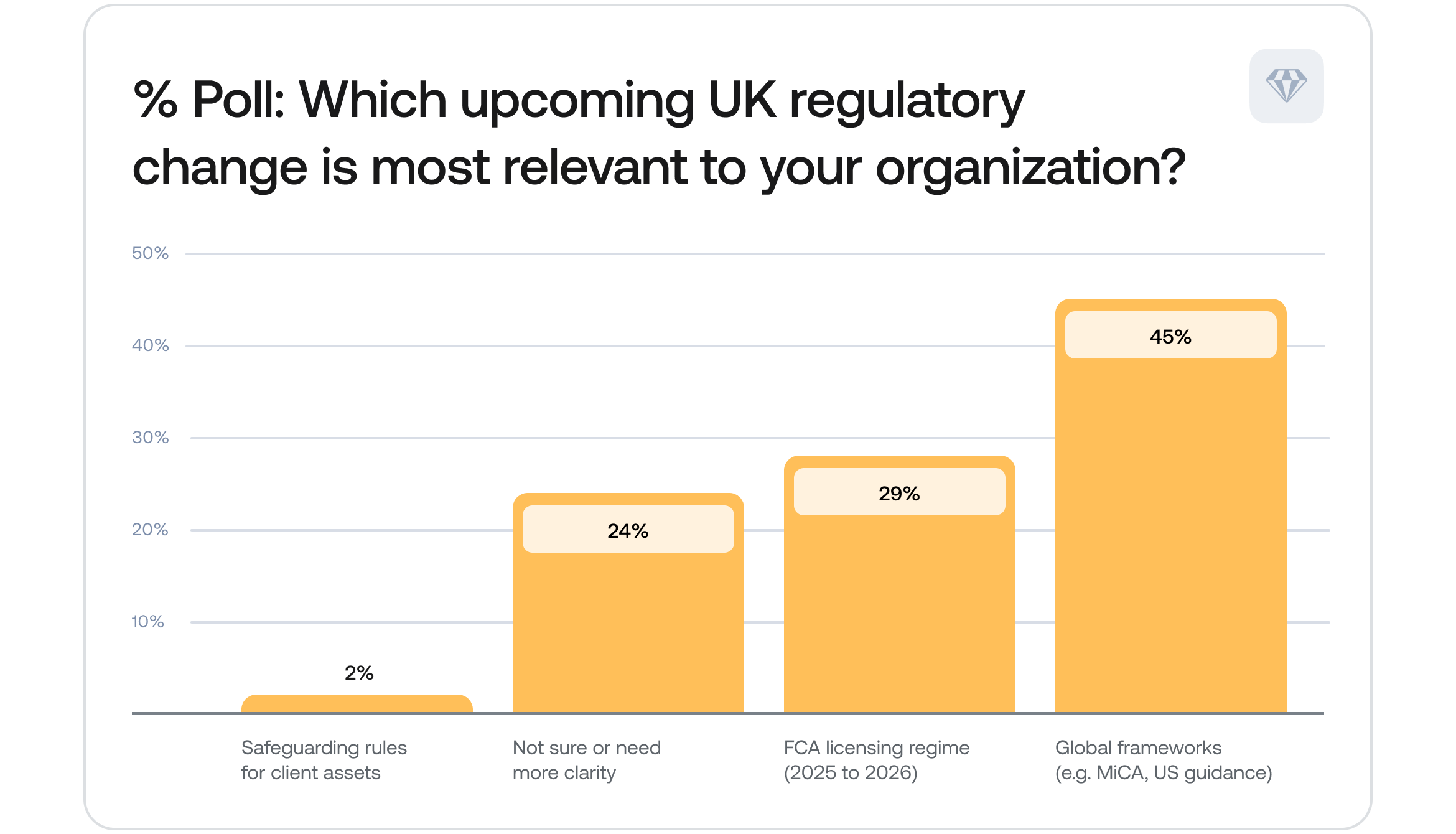

The poll below asked the audience which change was most relevant to them:

Almost 50% of the respondents saw global frameworks as most relevant to them, while nearly a quarter were unsure.

The US and EU Crypto regulations and jurisdictional arbitrage

Marina cited the UK and EU are difficult destinations for crypto exchanges and businesses to set up cost-wise and legally. This drives businesses towards more favorable crypto regulatory environments like the US, Dubai, and parts of APAC. She emphasized that expansion from one jurisdiction to another creates dynamic scenarios for which exchanges require guidance.

Regarding regulatory arbitrage, Clair spoke about MiCAR in Europe. She highlighted that although MiCAR applies throughout the EU, regional differences include that some states already have licensing processes while others do not. Additionally, different states can have transitional periods from three to six months.

Although she emphasized that the risks of regulatory arbitrage should be mitigated through guidance from the European regulator, they still exist. Pressed on where in the EU a young entrepreneur might best establish themselves, she suggested the Netherlands to expedite acquiring a trading license within a year, but Eastern Europe if they want to keep set-up costs low. She also noted the importance of choosing a jurisdiction with a proactive and knowledgeable regulator to provide clarity on compliance requirements.

How the UK and EU crypto regulatory frameworks address red tape

Dima then spoke about the prevailing climate of competition as different countries and jurisdictions jockey to become crypto hubs. He added that the new UK legislation intends to remove much of the red tape that hampers new business.

On this subject, Sam referred to the UK’s March 2025 action plan for the next five years, which included fit-for-purpose regulations for the crypto industry, quipping that the “Dear CEO” letters of the past have been abandoned going forward. This signals a shift towards removing red tape for all entrepreneurs in the UK, not just crypto ones, which is a move in the right direction.

Clair then highlighted the issue of red tape in the EU, specifically in the context of the accelerating deregulation in the US. She acknowledged that crypto businesses in the EU raise their voices about red tape. Still, she said EU regulators want a solid regulatory foundation that fosters innovation without harming consumers or exposing them to fraud.

Addressing how Crystal Intelligence meets its clients’ risk assessment and AML/CTF needs across different jurisdictions in the current climate, Marina pointed out that adherence to the FATF recommendations is the bottom line regardless of regional regulatory variations.

She acknowledged the multiple moving parts of any AML/CTF compliance regime, including incorporating KYC service providers, customer data, filing SARs, and engaging with regulators. This creates a challenge for individual firms, who might need solutions from several sources.

Predictions of how the new UK crypto regulatory regime will take shape

Dima recognized the challenges regulators face when designing and implementing a framework to govern such a shape-shifting and dynamic industry. He used the example of the current trend of differentiating between cryptocurrencies and stablecoins, a distinction barely made a year ago.

Sam acknowledged that the UK regulators have yet to achieve the granular detail of the regime’s design. However, he praised the ongoing efforts to reduce red tape and make the UK a more attractive hub for crypto businesses.

Clair said that regulators in the EU meet the requirements of the current market but can be reactive rather than proactive about change. She highlighted that regulators must amend legislation to adapt to the evolving crypto ecosystem as challenges arise.

Marina pointed out that the experience of MiCAR implementation is unlikely to be repeated in the UK because of how long it took to implement, and that for a dynamic industry, you need dynamic supervision and dynamic regulation. She also spoke highly of the efficiency of VARA in the UAE but cautioned that the Dubai-based regulator’s activities were not likely to be imitated in Europe or the UK because of the many resources VARA applies to maintaining its regime. Ultimately, she highlighted the importance of a hyperlocal strategy within specific jurisdictions for businesses to best protect themselves.

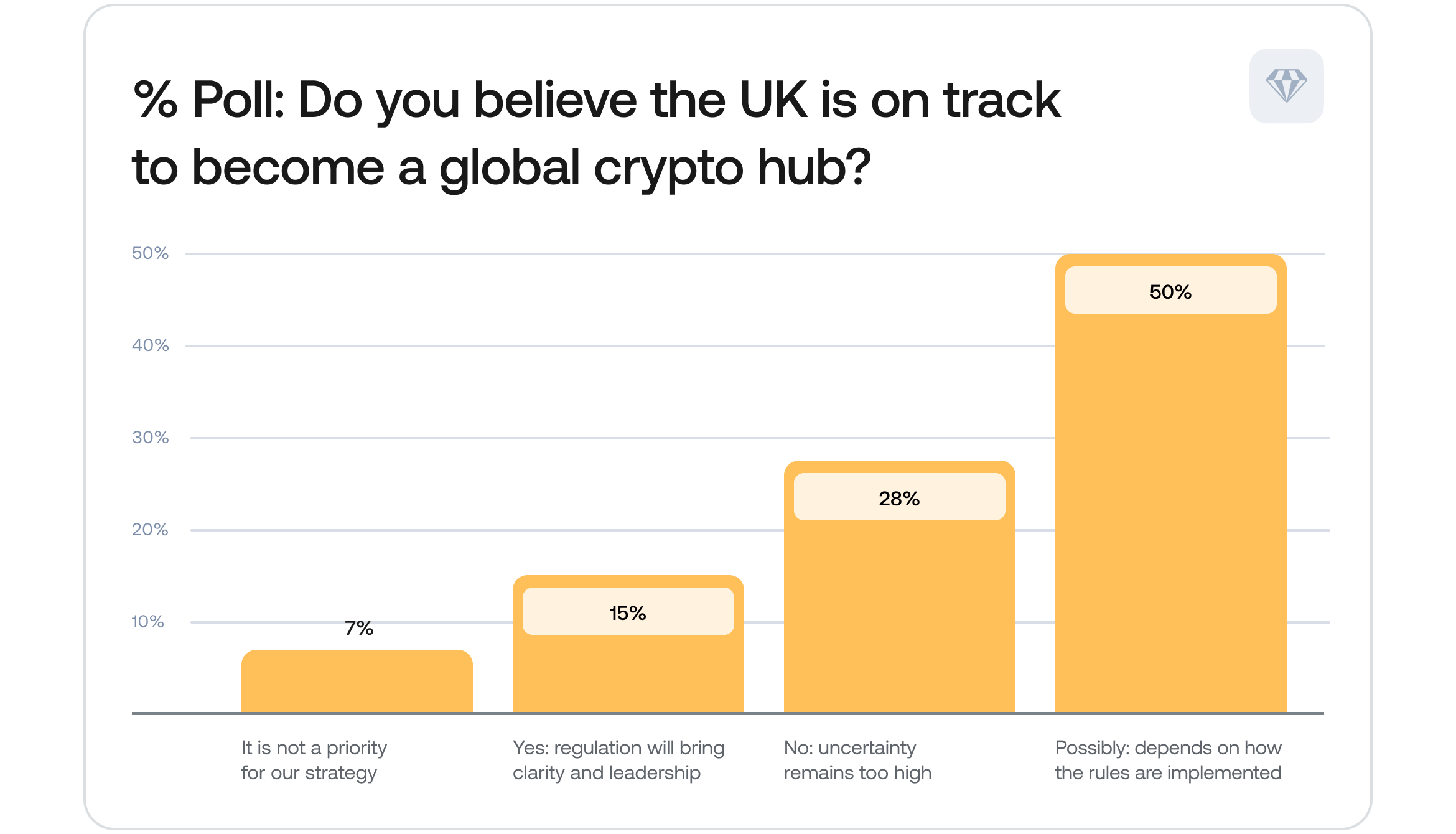

The poll below asked the audience if they believed the UK could become a crypto hub:

50% of respondents thought it was feasible, while 28% were emphatic that it was not.

Conclusions on the UK crypto regulatory framework

Marina said it is incumbent upon crypto industry role-players to help educate regulators on how the crypto ecosystem currently works and will develop. She encouraged crypto businesses to interact candidly with the regulators in the jurisdictions where they intend to operate to achieve this. She also suggested that the same issue will likely bedevil AI integration into the mainstream financial framework.

Clair was positive about developments in the UK and encouraged greater synchronization of regulatory frameworks globally, not only in the US, UK, and EU.

Sam expressed excitement at the UK Finance Minister’s announcement and was positive about watching the developments during 2025.

Dima closed by saying that the UK could leverage being behind the EU crypto regulatory framework to avoid some of the pitfalls EU regulators encountered. Finally, he expressed his belief that long-term investment in risk management, including compliance, is the best practice within the fintech industry and welcomed the inception of regulatory clarity from the UK Treasury.