Crystal Foresight tracks on-chain flows, holder distributions, and realized returns across 99% of the stablecoin market. This week: sUSDe and sUSDS together hold $7.7B and have generated roughly $545M in returns since launch. We traced each token address by address to see who actually collected.

Key takeaways

The returns are real, but almost none reached retail savers. sUSDe has generated about $406M in realized gains – meaning gains that have been booked and have changed hands – and sUSDS about $140M. Identifiable protocols and intermediaries captured roughly $425M of that combined total. Direct retail wallets, those holding under $100k of either token, realized $2.4M on sUSDe and $0.6M on sUSDS.

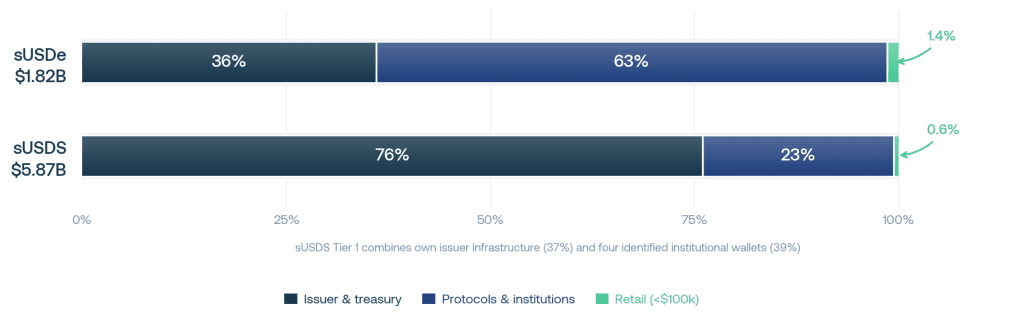

Both tokens look broadly held until you check a layer down. sUSDS tracked supply is $5.9B against sUSDe’s $1.8B. Strip out each token’s own issuer infrastructure and four mega-whale wallets from sUSDS, and the gap between their ordinary holder bases collapses to 1.2 times. Direct retail holds 1.4% of sUSDe and 0.6% of sUSDS in dollar terms.

The biggest single earner is a derivatives market, not a savings pool. Pendle, a protocol that splits yield tokens into a fixed-rate leg and a leveraged-yield leg, captured just over half of sUSDe’s total realized gains – about $204M. Three-quarters of those gains went to wallets that have each moved more than $10M on-chain across their full history.

One group of operators runs the entire stack. The top Pendle yield-token holders also appear in Aave, Morpho, and Sky lending datasets simultaneously. Two hold direct Ethena redemption rights – a route gated to vetted, institutional counterparties and available only by application.

Both yields rest on the same underlying bet. sUSDe’s rate comes from shorting crypto perpetual contracts. Sky’s Savings Rate, as last week’s analysis of Spark collateral showed, is funded largely by lending against ETH and other crypto assets – not Treasury bills. The same operators, comfortable with that exposure, recur across both tokens.

Market snapshot

sUSDe (Ethena) | sUSDS (Sky) | |

|---|---|---|

Tracked supply | $1.82B | $5.87B |

Own issuer infrastructure | 36% of supply | 37% of supply |

Mega-whale share (4 wallets) | Under 7% | 39% ($2.27B) |

Direct retail (<$100k) | 1.4% ($24M) | 0.6% ($36M) |

Realized returns to date | $406M | $140M |

Retail realized gains | $2.4M | $0.6M |

Current APY (on-chain) | ~4.2% | ~3.6% |

All figures from Crystal Intelligence on-chain analytics as of June 2026.

The pitch

Ethena markets sUSDe as a dollar-denominated savings instrument accessible to anyone, describing it as an internet bond that earns the protocol’s yield. Sky markets sUSDS as an automatic savings token with no fees and full liquidity. In April 2026, sUSDS became the first on-chain DeFi product to receive a credit rating from S&P: a B-.

The implied user in both products is an individual parking dollars to earn a return – the same way they would in a savings account.

Both tokens run on public blockchains. That means the holder distribution and the return flows are verifiable, address by address. We ran that analysis across the full holder and return population. The answer is more specific than the pitch.

Who holds them

sUSDS appears roughly three times larger than sUSDe at first glance. Once you separate genuine holders from protocol machinery, that gap almost disappears.

Two tiers carry nearly all of Sky’s lead. First: issuer infrastructure. Nine Spark and MakerDAO contracts, spread across three chains, hold $2.17B of sUSDS – 37% of tracked supply. These are operational and treasury contracts controlled by the issuer, not independent investors. Second: four unnamed mega-whale wallets holding $2.27B between them, in positions ranging from about $145M to over $1.1B each. Those are institutional treasury positions.

sUSDe has its own issuer vault, holding about $650M. Its largest unlabeled single wallet sits just under $120M – a fraction of sUSDS’s whale tier.

Remove both sets of outliers and the comparable ordinary-holder base is $1.43B for sUSDS and $1.17B for sUSDe. A gap of 1.2 times.

Below that level, both bases thin quickly. Direct retail wallets – those holding under $100k of either token – account for $24M of sUSDe and $36M of sUSDS. Combined, that is under 0.8% of the $7.7B total. The largest non-infrastructure category across both tokens is itself an intermediary layer: Aave holds $248M of sUSDe, Morpho $181M. These are lending markets – they hold the token on behalf of users a layer further down. A holder count that stops at Aave addresses stops too soon.

Who earns

Returns concentrate where the holdings do.

On sUSDe, Pendle’s derivatives markets booked $204M in realized gains – just over half of the token’s $406M total. Aave follows at $57M, then Ethena’s own vault at $26M. Identifiable protocols and intermediaries captured about $345M. Direct retail realized $2.4M.

On sUSDS, Sky’s own Spark infrastructure is the largest single earner at about $29M. The largest outside earner is a competitor: Ethena appears to have allocated roughly $2.2B of reserves into Sky’s vault during the high-rate window of late 2024 and exited with $25M in returns. That position traces to a single treasury wallet – Ethena’s Coinbase address, identified via Etherscan. Identifiable protocols and intermediaries captured about $80M of sUSDS’s $140M total.

Outside the protocol layer, the visible winners are funds. An address attributed to Abraxas Capital – the macro fund whose near-$3B ETH position at SparkLend featured in last week’s analysis – cycled a near-billion-dollar sUSDe position and booked $4.65M. A 0.5% return earned on size.

The base churns fast. Eighty-eight percent of sUSDe addresses and 72% of sUSDS addresses have already fully exited.

Inside the biggest earner

Pendle is not a savings pool. It is a derivatives venue. Where Aave works like a lending market – deposit sUSDe, earn interest, hold the underlying at all times – Pendle splits the token in two. The first component is a principal token: a fixed-rate instrument redeemable for the underlying at a set future date, bought at a discount. Pay roughly $0.92 today, redeem for $1.00 at maturity. The rate is locked, the outcome is predictable, and the token behaves like a short-term bond.

The second component is a yield token: it collects all of sUSDe’s yield up to that same maturity. A small position in yield tokens commands the yield from a far larger underlying balance – a leveraged bet on whether Ethena’s funding rate stays elevated.

When we look at yields by claim size it can look dispersed: of roughly $185M claimed across some 9,400 addresses, the top 50 took half and 79% went to wallets collecting more than $100k each – led by a single Gnosis Safe at $8.7M – with thousands more claiming under $100k apiece. But a small claim does not necessarily indicate a small player.

Segment instead by lifetime on-chain volume – how much total value each wallet has moved across its full history – and the picture changes. Wallets that have each cycled more than $10M on-chain took three-quarters of the yield – a concentration no story about passive savers can explain. Active traders and smaller funds, with $1M to $10M of lifetime volume, took about 15%. Wallets whose entire on-chain history runs under $1M took under a tenth.

The biggest yield-token holders are not Pendle-specific. The same wallets carry SparkLend loans, Aave and Morpho positions, and Sky vault deposits simultaneously. Two hold direct Ethena redemption rights – a route available only to verified institutional counterparties. One group of operators, running the full on-chain lending and derivatives stack at once.

Pendle is the largest box, not the only one. The same logic runs through Aave and Morpho – the two biggest third-party holders of sUSDe – where a gain booked at the lending contract belongs to the wallets that supplied through it, and those wallets are just as traceable. We’ve started pulling those threads; mapping the lending layer in full is the next step in building out this picture rather than something we settle here.

Where the yield comes from

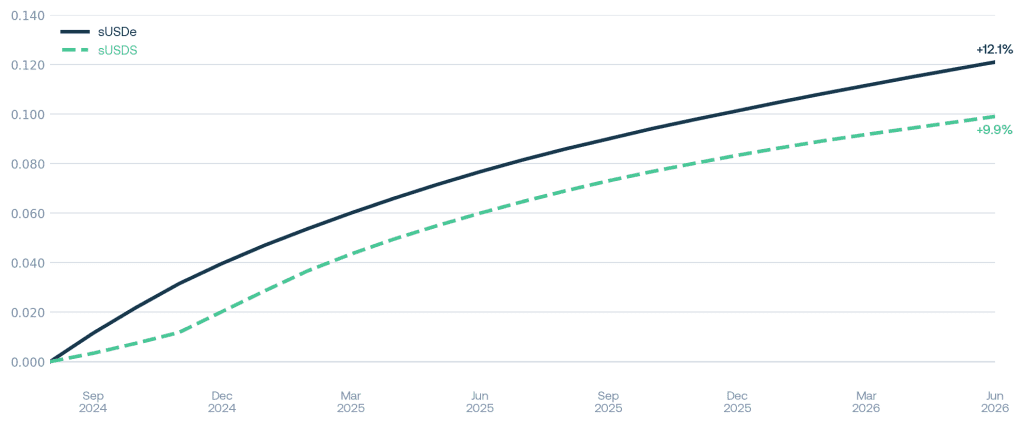

The two rates behave differently on the surface. sUSDe’s yield is a market rate: the funding income Ethena collects by shorting crypto perpetual futures contracts – instruments where traders pay a continuous fee to hold leveraged long crypto positions – as a hedge against its dollar-pegged collateral. That rate peaked near 55% in early 2024 and sits at about 4.2% today.

sUSDS’s is a governance decision: the Sky Savings Rate, pushed to 12.5% in December 2024 and cut in steps to about 3.6% now.

Over their common history from September 2024, sUSDe has returned 12.1% cumulatively and sUSDS 9.9%. A modest premium for sUSDe’s higher rate volatility.

Both rest on the same underlying bet. Ethena’s yield comes from demand to be long crypto perpetuals. Sky’s Savings Rate, as last week’s SparkLend analysis showed, is funded substantially by lending against ETH and other crypto collateral – not by Treasury bills. Underneath, both rates depend on the same market condition: sustained demand for crypto leverage.

That shared exposure is why the same operators recur across both products. A leveraged yield-token position at Pendle stacked on top of sUSDe is simply a leveraged version of that same crypto-demand wager.

The pattern

Both tokens deliver their stated promise. Deposit and hold, and the exchange rate moves upward.

What the on-chain record adds is proportion. The headline supply is mostly issuer infrastructure and large holders. Returns flow to the protocols built on top. Inside the biggest of those protocols, the holders are institutional too – with one recurring group running positions across the entire stack. Retail is present mainly as headcount, not as money.

This is the second consecutive week with the same structure. Last week: a dollar marketed as decentralized resolved, one layer down, into a governance-issued credit line and a dominant institutional fund. This week: savings tokens marketed broadly are held and earned from almost entirely by institutions.

As banks move into tokenized deposits and the line between a bank account and an on-chain token becomes less clear, that check becomes more consequential – not less. The pitch says savings for everyone. The chain shows who is actually there.

Data as of June 2026. All figures derived from Crystal Intelligence on-chain analytics and Dune Analytics (crystal_intelligence). Holder and gains analysis covers the full population of mainnet holders; each issuer’s own infrastructure is identified separately. sUSDS figures include Arbitrum and Optimism holders, with bridge escrows netted out. All figures are approximate. This report is for informational purposes only and does not constitute investment advice.