Key takeaways

- Texas ranks second nationally in crypto crime losses. The FBI’s 2025 Internet Crime Report puts Texas at $1B in crypto-linked losses, behind only California ($2.1B) and ahead of Florida and New York.

- The state’s permissive licensing posture predates the current threat profile. Texas Department of Banking Supervisory Memorandum 1037, in force since 2014 and revised in January 2025, holds that non-stablecoin centralized virtual currencies are not money under the Texas Finance Code.

- Federal law is raising the floor. The GENIUS Act actively creates state supervisory roles for stablecoin issuers, while the CLARITY Act, still before the Senate, preserves existing state anti-fraud authority rather than adding to it. In both cases, consumer-facing enforcement falls to state agencies.

- The capability gap is solvable. Texas already has institutional players, but is arguably missing investigative training in blockchain forensics and operational access to professional-grade analytics tools.

Texas leads the country on crypto policy. Has its enforcement capacity kept pace?

Texas leads the country on crypto policy. Has its enforcement capacity kept pace?

Texas leads the country on crypto policy. Has its enforcement capacity kept pace?

Texas leads the country on crypto policy. Has its enforcement capacity kept pace?In June 2025, Texas authorized a strategic Bitcoin reserve under state custody, making it the third US state to pass such legislation, and the first to actually buy Bitcoin for the digital asset store in November 2025. In July that year, President Trump signed the GENIUS Act into law, the first US federal framework for payment stablecoins. Meanwhile, the FBI’s Internet Crime Complaint Center (IC3) recorded that Texas residentslost just over $1B to crypto-linked fraud in 2025, the second-highest total of any US state.

Texas is one of the most permissive states towards crypto. It also has the second-largest crypto crime loss profile in the country. Those two facts are not in tension: They are the same story.

The federal floor is rising fast. The state’s framework, calibrated for a smaller and more concentrated crypto economy, is not moving as fast, and the consequence is that state law enforcement and state regulators inherit the fallout.

What does the Texas regulatory framework actually require?

Texas regulates virtual currency through the Texas Department of Banking under Chapter 152 of the Texas Finance Code. The operative interpretation: transmission of virtual currency alone is not money transmission.

A license is required when virtual currency is exchanged for sovereign currency, and the operator acts as a third-party intermediary. Stablecoin transmission may independently trigger licensing where the stablecoin qualifies as money or monetary value under the statute.

The legislature has built incrementally on top of this base:

- A 2021 amendment recognized virtual currencies as commercial property under Texas commercial law and clarified how digital asset rights can be transferred.

- A 2023 amendment introduced proof-of-reserves requirements for digital asset service providers – the first such requirement in the country.

- Most recently, SB 21 (signed June 20, 2025) established the Texas Strategic Bitcoin Reserve under the Comptroller’s custody, eligible to hold crypto with a 24-month average market capitalization above $500B. At signing, Bitcoin was the only qualifying asset.

The combined picture is permissive at the boundary, supervisory in the middle, and policy-forward at the top.

Crypto adoption rates in Texas

Texas’s likely crypto adoption is high in absolute terms, reflecting the state’s large population, crypto-friendly environment, and its standing as the second-largest state economy.

Internal Revenue Service tax data from 2022 analyzed by SmartAsset found that crypto adoption trends were strongest in Western States, led by Washington (2.43% or 91,310 households surveyed), and weakest in the South, led by West Virginia (0.84% or 6530 households). Although Texas ranked sixteenth overall, with an estimated adoption rate of 1.78%, the 242,280 households involved in crypto in 2022 ranked the state second in the US, behind only California (416,340 households).

Meanwhile, the National Cryptocurrency Association 2026 Annual State of Crypto Holders report found that 38% of American crypto holders resided in the sixteen-state South region, of which Texas is the most populous.

Key trading infrastructure available to Texans

All major US-based crypto exchanges: Most major US retail exchanges are available in Texas, including Coinbase, Kraken, Gemini, Robinhood, Crypto.com, and OKX. Two notable exceptions are Binance.US and Bitstamp, which are both unavailable to Texas residents due to state regulatory restrictions.

Peer-to-peer trading marketplaces: Texas peer-to-peer crypto access is narrow: Bisq (decentralized and non-custodial) is fully accessible with no state-level jurisdictional intervention, while LocalCoinSwap and RoboSats permit US residents, including Texans. The absence of major players such as BinanceP2P is likely due to regulatory requirements and enforcement actions at both the federal and state levels.

Over-the-counter (OTC) desks: Major OTC services are accessible to Texas residents, including Coinbase Advanced OTC, Kraken OTC, and Gemini eOTC.

Crypto ATMs: Texas hosts approximately 4,000 live crypto ATMs, the highest number in any US state. Major operators include Bitcoin Depot, Coinstar/Coinme, and Cryptobase.

Crypto-focused banking services: The dedicated crypto banking landscape in Texas is limited. United Texas Bank (Dallas) has historically served crypto businesses and completed an OCC national bank charter conversion in May 2026, positioning it as a crypto-infrastructure banking provider. Nationally available crypto-adjacent banking options accessible to Texas residents include Mercury (business accounts with crypto exchange rails), Customers Bank, and Ally Bank. No Texas-chartered retail bank currently offers integrated crypto custody to retail customers.

How does federal law impact Texas oversight?

The GENIUS Act was signed by President Trump on July 18, 2025. It requires federal regulators to issue final implementing regulations for stablecoin issuers, and the statutory framework explicitly contemplates state regulators supervising state-chartered stablecoin issuers under approved state regimes. The CLARITY Act, the House-passed market structure bill now before the Senate, will centralize digital asset regulation federally, while states will retain their existing anti-fraud authority over securities.

For Texas, three practical implications follow.

- The Texas Department of Banking will inherit most supervisory responsibilities that the federal floor does not directly perform, with support from the Texas State Securities Board. State-chartered stablecoin issuers with under $10B in outstanding issuance, and state-licensed money services businesses handling digital assets, both flow back to state-level supervision – the former under the GENIUS Act framework, provided Texas obtains federal certification of its regulatory regime.

- The form of consumer-facing fraud enforcement remains unchanged. Pig-butchering, crypto ATM fraud, investment scams, and elder financial exploitation are already prosecuted at the state level. The federal floor does not change the enforcement reality. It compresses the timeline.

- The analytical capability required to run these supervisory and enforcement functions must be blockchain-native. The investigative skill set that helped prosecute bank fraud in 2010 is not the skill set that helps prosecute a Tron-based pig-butchering ring in 2026.

How big is the Texas crypto crime problem?

In 2025, Texas residents reported approximately $1B in crypto-related losses to the IC3, the second-highest of any US state. Texas’s 22% year-on-year rate of increase in crypto-related dollar losses parallels the national rate[NB1], and the state accounts for nearly 9% of all reported US crypto losses.

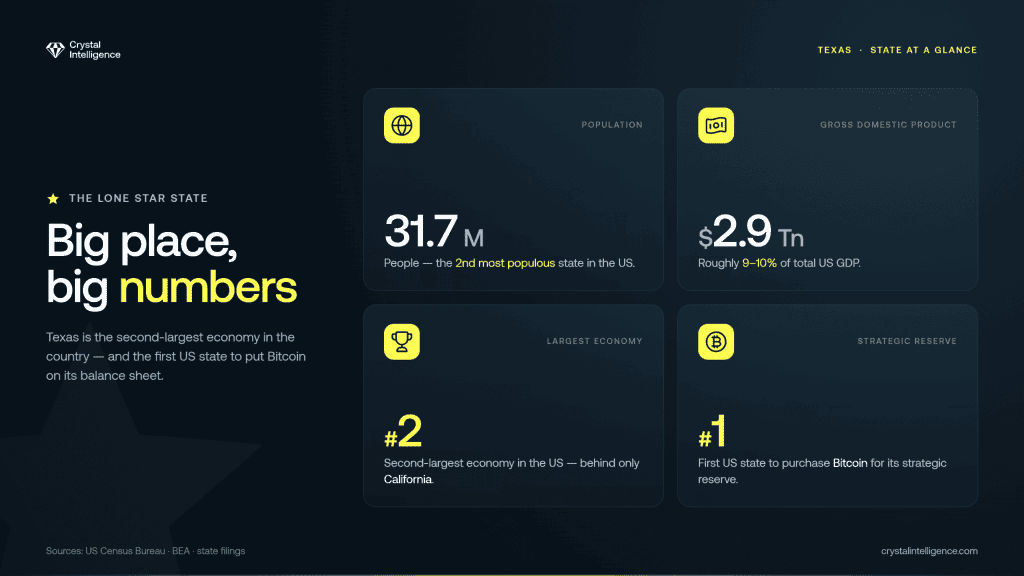

Similarly, Texas’s estimated 2025 GDP of $2.9Tn is second only to California and accounts for a 9-10% share of US GDP, while its estimated 2025 population of 31.7 million is also about 9% of the US population.

The age breakdown in those affected by crypto crime is the harder number.

Nationally, Americans 60 and older filed 44,555 crypto complaints and reported $4.4B in losses in 2025, up 56% year over year. In absolute terms, Texas has one of the largest senior populations of any US state, with more than 6 million residents being over the age of 60. Pig-butchering, investment fraud, recovery scams, and crypto ATM fraud often target this demographic.

Crypto ATMs specifically are now a top FBI focus area, and the IC3 issued a dedicated public service announcement on crypto ATM complaint data in May 2026. It showed that Texans lost $56.8M to crypto ATM fraud in 2025, the highest of any state, and suffered 14.6% of the national total losses, which amounted to $389M.

What should Texas law enforcement and regulators focus on

Three priorities are emerging consistently across the most active state-level crypto enforcement programs in the country.

- Build blockchain investigative capability at the case-officer level. The bottleneck on most state-level crypto prosecutions is not legal authority. It is the investigator’s ability to trace funds across chains, attribute wallets to entities, and produce court-admissible evidence.

- Deploy professional-grade analytics to active investigations. Most state agencies investigating crypto cases today are operating with consumer-grade tools or relying on external contractors for individual cases.

- Share data. Coordinate state regulators with state law enforcement on a common analytical baseline. The Texas Department of Banking, the Texas State Securities Board, the Texas Attorney General’s Consumer Protection Division, and the Computer Information Technology and Electronic Crime Unit (CITEC) will, between them, handle most of the crypto compliance and enforcement activity in the state. Operating on the same data, the same entity attributions, and the same investigative tooling materially reduces friction across these handoffs.

Frequently asked questions

Does Texas require a money transmitter license to operate a Bitcoin ATM? Under Supervisory Memorandum 1037, virtual currency transmission alone is not money transmission under Texas law. A money transmitter license is generally required where the ATM operator exchanges crypto for fiat as a third-party intermediary. Practitioners should consult the latest Department of Banking guidance for case-specific application.

Has the Texas Strategic Bitcoin Reserve changed crypto enforcement? Not directly. SB 21 creates a state asset holding mechanism under Comptroller custody and is administratively separate from the Department of Banking, the Texas State Securities Board, and state law enforcement. The Reserve’s existence does, however, signal a policy posture that will influence rulemaking and resource allocation in adjacent areas.

What does the GENIUS Act mean for Texas-licensed money services businesses? The GENIUS Act creates a federal framework for payment stablecoin issuers and contemplates state-level supervision under approved regimes. Texas money services businesses that issue, handle, or settle stablecoins should expect increased coordination between federal rulemaking, the Texas Department of Banking, and the Texas State Securities Board.

Is crypto ATM fraud a particular problem in Texas? Yes. The FBI’s 2025 Internet Crime Report and the May 2026 IC3 PSA on crypto ATM complaint data both identify ATM fraud as a growing national pattern, and Texas recorded the highest adjusted ATM fraud losses of any US state in 2025 at $56.8M.

What does effective crypto law enforcement training look like? Effective programs combine blockchain fundamentals, wallet attribution and clustering methods, cross-chain tracing across the major networks (Bitcoin, Ethereum, Tron, Solana, BNB Chain), evidence preservation, and prosecutor-facing report production. Crystal’s training programs are built around this curriculum and delivered to state and local agencies in the United States and internationally.

Closing perspective

Texas has chosen, deliberately and publicly, to be one of the most crypto-forward jurisdictions in the United States. That choice carries a corresponding responsibility, which is to build the enforcement and supervisory capacity that the policy posture implies. The federal floor is rising fast, and most of the practical work of supervising stablecoin issuers, prosecuting pig-butchering rings, and protecting senior Texans from ATM fraud will be done at state level.