Crystal Foresight tracks stablecoin flows, institutional capital movements, and on-chain fixed income instruments. The tokenized Treasury market has passed $15B. This analysis uses on-chain data to show how two leading products work in practice – and who is using them. This blog is part of Crystal’s ongoing series tracking the financial system being built on-chain.

Key takeaways

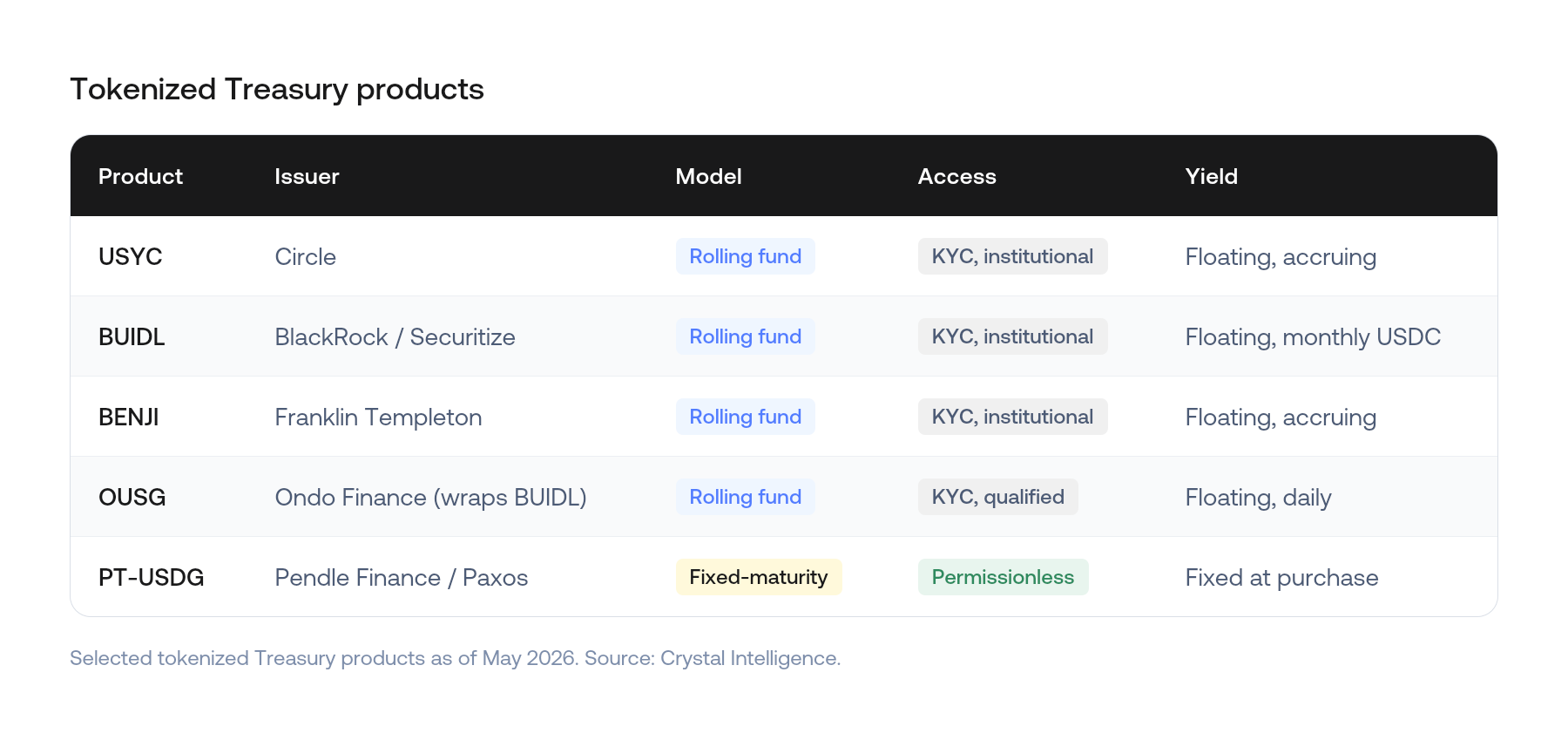

- The tokenized T-bill market has passed $16B, built on two architectures. Rolling funds (BlackRock BUIDL, Circle USYC, Franklin Templeton BENJI, Ondo OUSG) offer continuous yield with no maturity date. Fixed-maturity instruments (Pendle Finance pools) lock a rate at a specific date. Both settle on-chain in seconds.

- BUIDL holds $2.5B across just 90 addresses – average position $27.9M. Crystal’s analysis finds most long-term holdings sit on Avalanche rather than Ethereum, despite Ethereum processing $4.9B in subscriptions.

- The PT-USDG pool on Pendle peaked at $231.6M, built by institutional-scale deposits including $51.7M in a single day. The build-up pattern is periodic large blocks over several weeks – not retail accumulation. It settles on May 28, 2026.

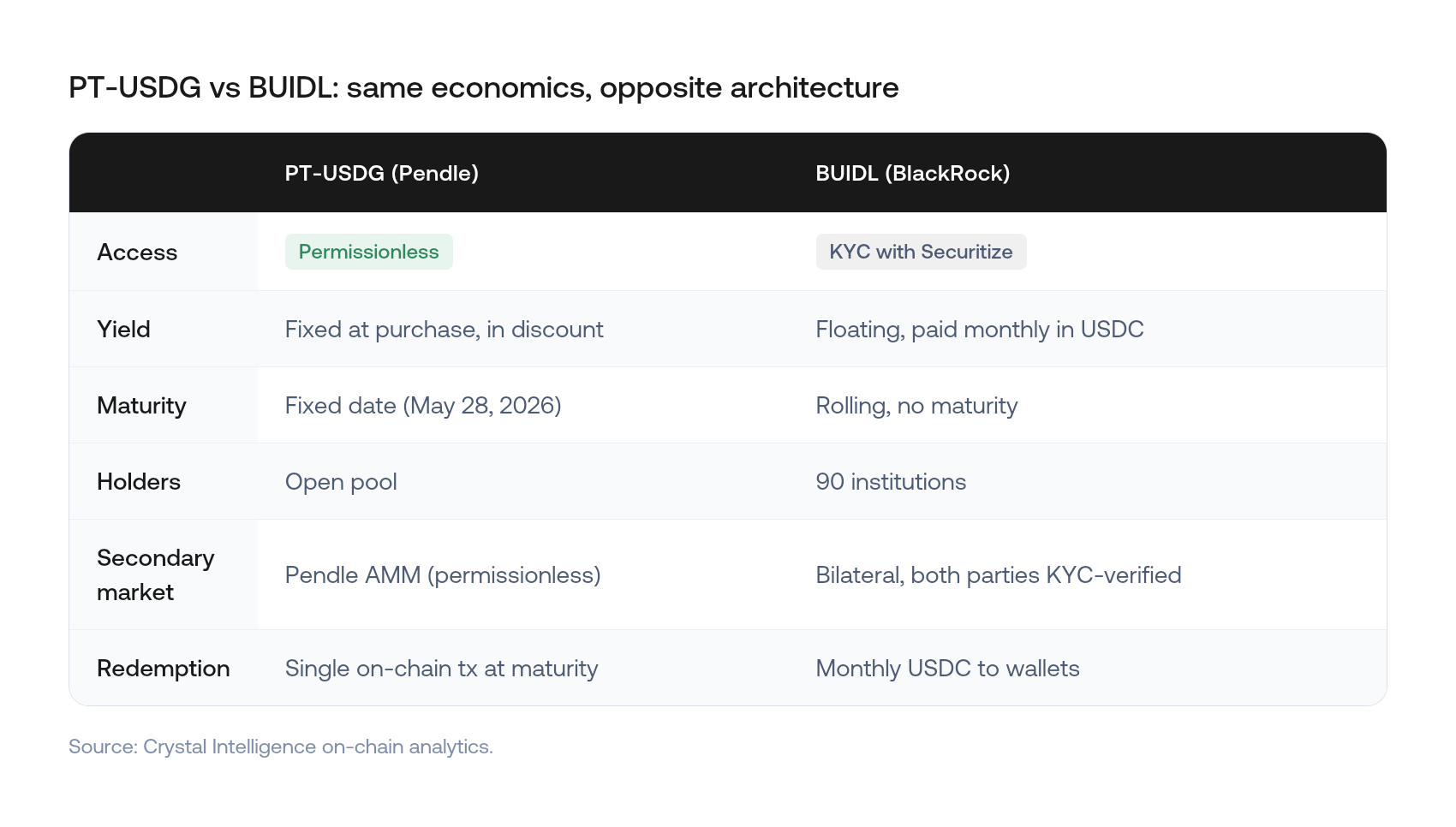

- The two models serve different needs, but the underlying economics are identical. The difference is in access, risk layers, and who can participate. For compliance teams and institutional allocators, the choice between permissioned and permissionless carries distinct operational and counterparty implications.

What tokenized T-bills are

A Treasury bill is the US government’s short-term debt. Buy at a discount, receive face value at maturity – the difference is your return. The concept is not new. The US Treasury established a framework for stripping bonds into principal and yield components in 1985. What is new is putting that settlement on a blockchain: seconds instead of days, publicly auditable, and usable as collateral without transferring it.

Two architectures account for most of the roughly $16B market.

Rolling funds work like on-chain money market funds. Investors subscribe, earn a floating yield that tracks short-term Treasury rates, and redeem when they choose. Access requires KYC (know your customer) verification. Circle’s USYC, BlackRock’s BUIDL, Franklin Templeton’s BENJI, and Ondo’s OUSG all follow this model.

Fixed-maturity instruments replicate T-bill mechanics more precisely. Buy at a discount, hold to a specific date, receive par at redemption. Pendle Finance builds these by splitting a yield-bearing stablecoin into its principal and yield components – the on-chain equivalent of STRIPS.

What Crystal’s data shows about PT-USDG on Pendle

The PT-USDG pool grew from zero to $231.6M in three months. The five largest single-day inflows account for over $143M. These are not retail-sized positions. The pool was built by a small number of participants making large, deliberate allocations over several weeks.

To understand why, you need to understand what USDG makes possible. Most stablecoins absorb the yield from their Treasury backing – Tether and Circle earn roughly the T-bill rate on a combined $267B in supply, and holders earn nothing. USDG, issued by Paxos, distributes that yield to its network partners instead. Pendle then splits USDG into a principal token (PT-USDG), redeemable for exactly $1.00 on May 28, 2026, and a yield token that captures all floating yield until maturity. Buy the principal token at a discount, and that discount is your locked return.

Three phases visible in the data.

The pool launched on February 23, 2026 near zero and grew in three distinct phases.

- Build-up (February to April): A small number of large deposits. The single largest inflow was $51.7M on March 19, 2026, when the pool stood at $107.4M. The following week brought another $27.9M.

- Convergence surge (May 1 to 16): $67.9M net flowed in, with $112.2M in gross deposits. The PT discount had nearly closed – buyers were earning only basis points on a short remaining duration. The reason to enter was certainty: a near-riskless dollar position with a known redemption date. The pool peaked at $231.6M on May 16, 2026.

- Orderly unwind (May 17 to present): -$17.8M net as participants exit ahead of settlement. Standard fixed-income behavior at maturity.

On May 28, 2026, Pendle’s smart contract redeems every PT-USDG at exactly $1.00 in USDG. The entire $213.8M converts in a single on-chain transaction.

What Crystal’s data shows about BlackRock BUIDL

BUIDL launched in March 2024 as an institutional money market fund holding US Treasury bills, cash, and overnight repo. Each token is pegged at $1 NAV with yield paid monthly as USDC to investor wallets. Securitize acts as transfer agent: both sender and receiver of any transfer must be KYC-verified.

Inside the holder base

Ninety holders. $2.5B in assets. Average position: $27.9M. The permissioning requirement produces this concentration by design. In 2025, counterparties moved in large, episodic blocks: $862.3M net in October, then $471M out in December as institutions repositioned at year-end. By 2026, the pattern has steadied. The largest single-month net swing has stayed under $80M on the original contract.

The chain split

Across both share classes, Ethereum is the largest single chain at $1.1B. But $887.8M of that is BUIDL-I, a separate institutional share class launched in December 2024 that operates as Spark Protocol’s reserve account. Spark cycled $1.3B into BUIDL-I in March 2025, redeemed most of it in October, then re-entered at $250-278M per month in early 2026.

For the original BUIDL contract, Avalanche is the dominant chain at $624.9M. Ethereum holds only $178.4M. Ethereum has processed $4.9B in original BUIDL subscriptions, but roughly 80% has since been redeemed or bridged. Long-term positions have settled on Avalanche, where sub-second finality suits large static holdings.

Infrastructure, not just yield

BUIDL has become load-bearing infrastructure for other products. Spark Protocol holds it as a reserve asset. Ondo Finance wraps it to create OUSG. Deribit accepts it as derivatives margin collateral – moving tokenized Treasuries from a yield product into market structure. One detail visible only in on-chain data: the Securitize DS Protocol gives BlackRock the technical ability to freeze wallets, force-transfer positions, and burn tokens. Across $8.9B in combined issuances and two years of operation, the compliance burn count is zero.

What the two models mean for different participants

The underlying economics are identical: T-bill yield, dollar denomination, short duration. The risk layers are not. A conventional T-bill carries US government credit risk. PT-USDG adds Pendle smart contract risk, Paxos issuer risk, and DBS Bank custodian risk. BUIDL adds Securitize platform risk and BlackRock operational risk.

For compliance teams, BUIDL’s permissioned registry means every counterparty is KYC-verified and the issuer retains enforcement tools – even if they have never used them. PT-USDG’s permissionless pool simplifies access but shifts counterparty diligence to the participant. For allocators, the choice may come down to fixed or floating yield, and whether the position needs to be composable in DeFi.

What to watch

PT-USDG settles on May 28, 2026. Whether the pattern repeats is the first question. A new Pendle USDG pool launched immediately would confirm institutional appetite at current yield levels. If the redeemed $213.8M exits on-chain entirely rather than rolling into a new pool, that suggests this was a one-time opportunity rather than an ongoing workflow.

For BUIDL, the signal is whether the holder base broadens beyond 90 addresses. Acceptance as derivatives collateral at Deribit was a step toward broader adoption. The next would be treatment as a cash equivalent in prime brokerage relationships – accepted from day one rather than requiring special approval.

The broader question is whether fixed-maturity and rolling-fund models end up on the same institutional balance sheet. The on-chain infrastructure for both now exists. Whether they are used together, at scale, is what the next 12 months will show.

Frequently asked questions

- What is a tokenized T-bill? A tokenized T-bill represents a claim on US Treasury bill economics as a token on a public blockchain. The underlying assets stay the same. What changes is settlement: seconds instead of days, and positions are publicly auditable.

- What is the difference between a rolling fund and a fixed-maturity instrument? A rolling fund has no maturity date – investors earn a floating yield and redeem when they choose. A fixed-maturity instrument locks a rate at purchase and returns par value on a specific date. Rolling funds suit cash management. Fixed-maturity instruments suit precise yield commitments.

- What does KYC-gated mean for BUIDL? Both sender and receiver of any BUIDL transfer must be verified through Securitize’s registry. No DeFi contract can hold BUIDL without individual approval. This limits the holder base to vetted institutional counterparties.

- What risks do tokenized T-bills carry beyond the underlying Treasury? Tokenized versions add platform risk (the tokenization provider), smart contract risk (the code governing the token), and custodian risk (the entity holding the underlying assets). These layers vary between products.

- What happens to PT-USDG on May 28, 2026? Pendle’s smart contract automatically redeems every PT-USDG at exactly $1.00 in USDG. The entire pool converts in a single on-chain transaction. No custodian instruction or clearing house is required.