Crystal Foresight uses on-chain data to track 99% of the stablecoin market, currently a $311B. This analysis draws on 18 months of DEX transaction data to answer a question the volume number alone cannot: who is actually behind stablecoin trading on decentralised exchanges?

Key takeaways

- A few thousand addresses are the market. On EVM chains (Ethereum and compatible blockchains), 0.17% of trading addresses move 63% of stablecoin volume (two-thirds of all trades); on Solana, 224 addresses move 58%.

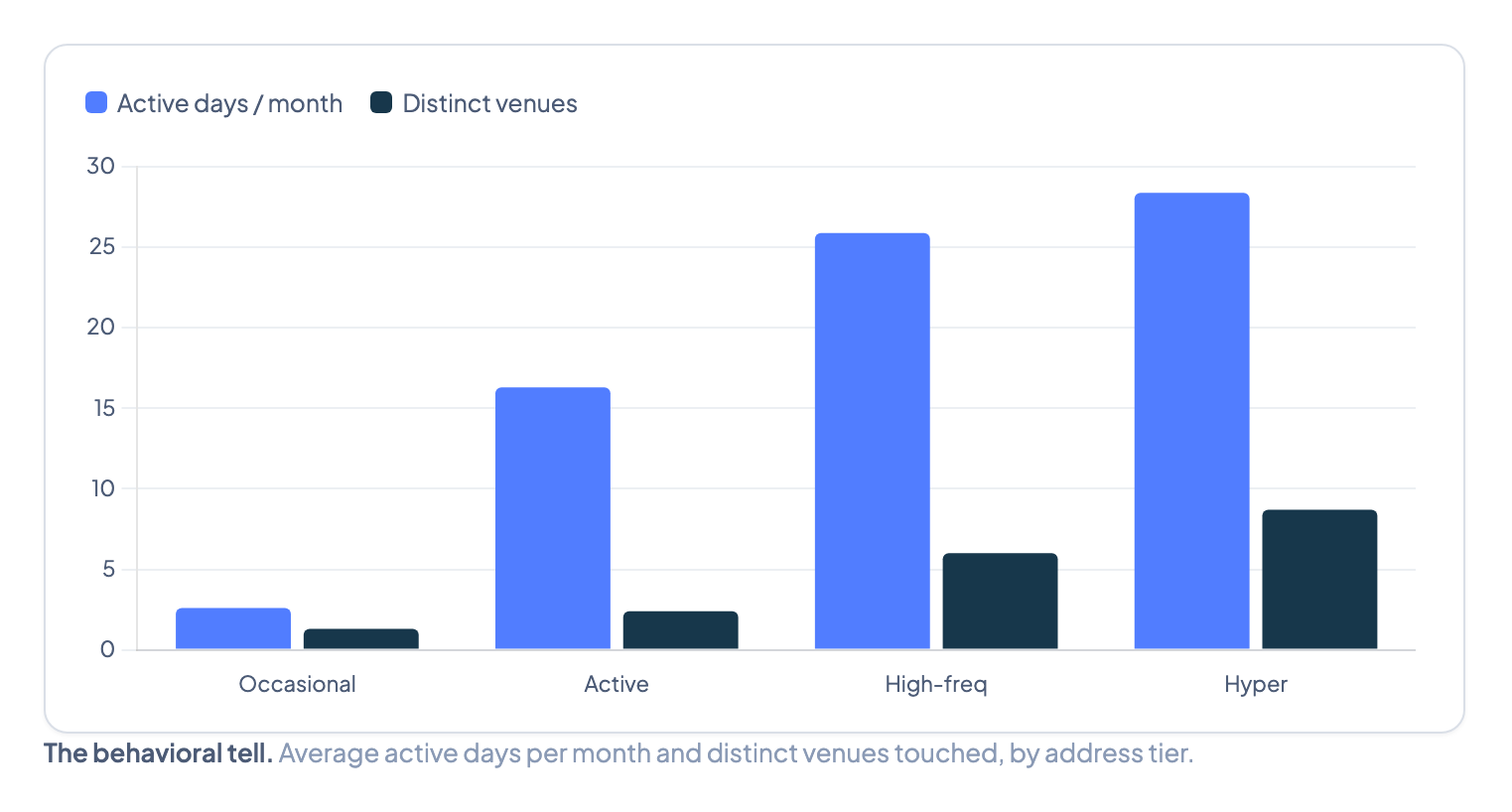

- You can read the player from its behavior. Machines trade almost every day across many venues; people appear a handful of days a month on one or two.

- The speculation is mostly machines. Automated addresses trade about 90% against volatile assets; ordinary wallets do proportionally more plain dollar-for-dollar swapping.

- Machines have dominated steadily. They have run about two-thirds of stablecoin DEX volume – about 65% – every month for a year and a half.

- What changed is the texture. Average trade size has collapsed roughly fourfold, the bot fleet has grown, and the venues moved to “proprietary AMMs” that have no website at all.

- And some of it leaves. About $0.15 of every bot dollar is swept to named exchange deposit accounts – Coinbase, Binance, OKX, Bybit – and the second-largest stablecoin trader on both chains is the market-maker Wintermute.

A top exchange that nobody visits

In December 2025, a venue called BisonFi opened and, within months, was handling a large share of all the stablecoin trading on Solana. It has no website, no app and no public face at all; you cannot visit it, and you cannot choose it. Orders reach it only when an aggregator quietly routes them there. That is not a curiosity at the edge of the market; it is close to what most stablecoin trading on a decentralized exchange (DEX, a trading venue that runs on blockchain code and records every trade publicly) now looks like. Which raises the question this analysis answers: if not people at a screen, then who?

The market in one breath

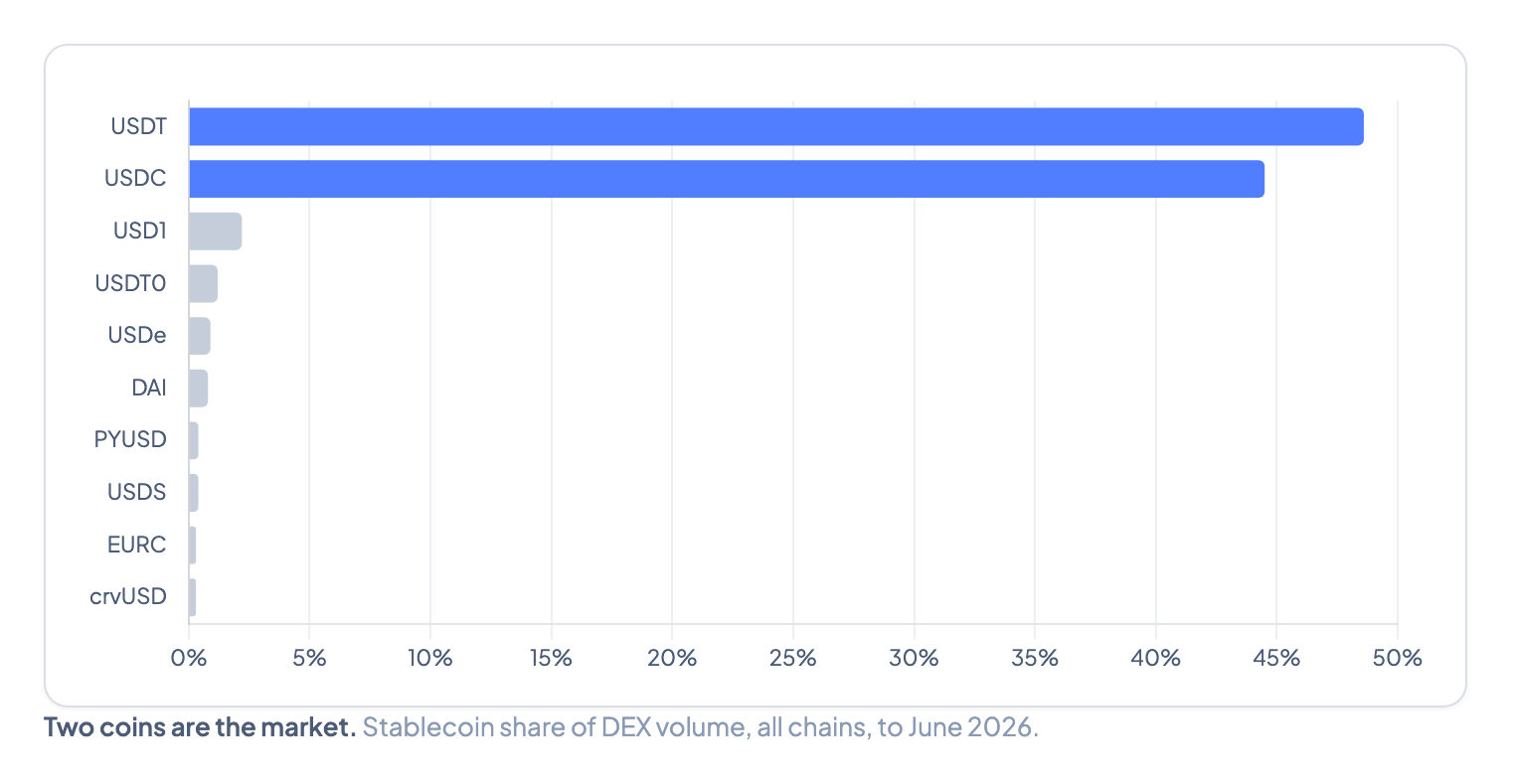

Two coins still are the market: USDT (about 48%) and USDC (about 44%) together account for about 93% of stablecoin DEX volume. The remaining stablecoins combined account for less than 7%. Total volume has fallen by about 70% from its late-2025 peak. But the number of trades has not fallen with it – and that gap is the first clue that the people you would expect to find here are mostly not the ones doing the trading.

Source: Crystal Foresight

Source: Crystal Foresight

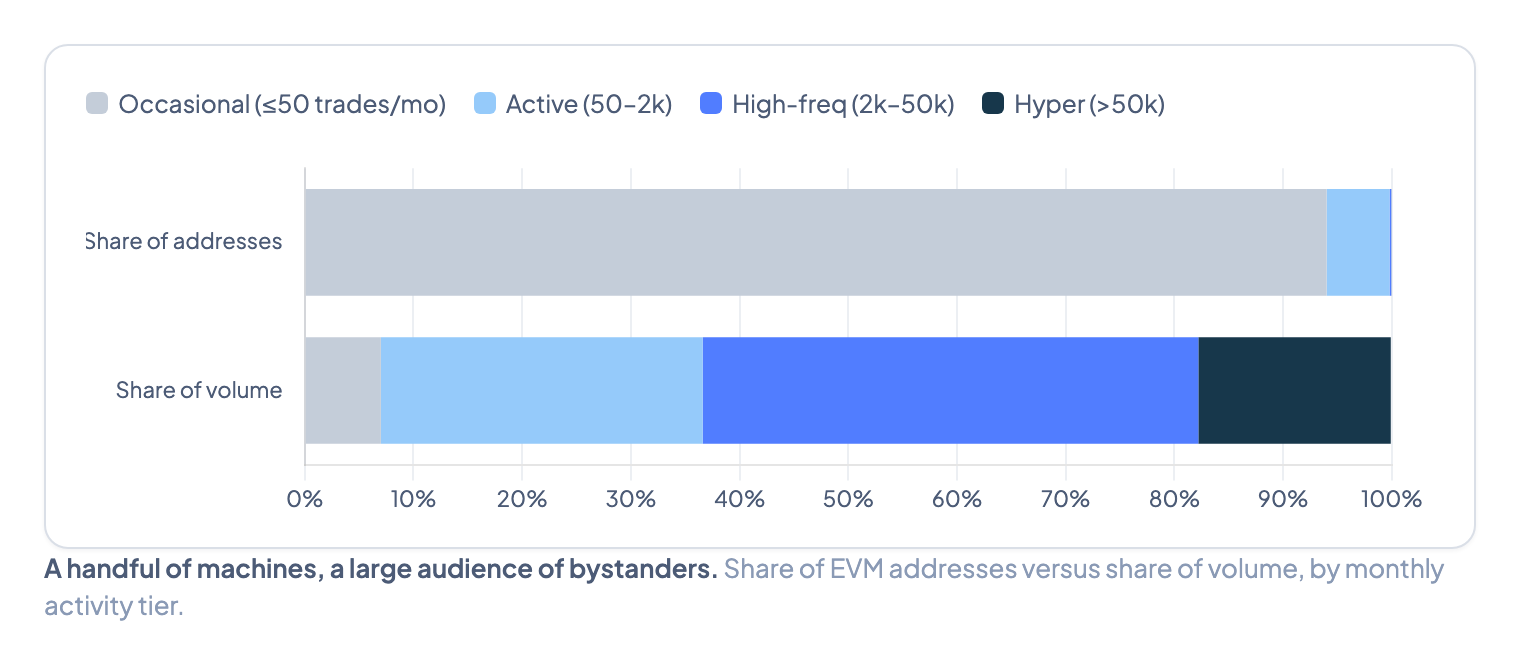

A few thousand addresses are the whole market

Group every trading address by how it behaves and the market turns out to be highly concentrated. On EVM chains in June, about 7,200 addresses – 0.17% of the 4.3 million that traded – accounted for 63% of stablecoin volume and two-thirds of all trades. The four million ordinary wallets, 94% of every address that touched a stablecoin, together did 7%. On Solana the point is sharper still: 224 addresses moved 58% of the volume.

This is not a market of many participants with a few whales. It is a small number of automated systems with a large population of occasional traders.

Source: Crystal Foresigtht

Source: Crystal Foresigtht

How to read a trader you have never seen

On a centralized exchange, you cannot see who is on the other side. On decentralized exchanges, you can – not by name, usually, but by behavior. Three kinds of traders show up, each with a recognizable signature.

Individuals are the four million in the tail. They trade on one or two venues, a couple of days a month, in amounts from tens to a few thousand dollars. Sporadic, low-volume, human-paced.

Professionals are firms that trade for a living: market-makers and cross-chain bridges. They are the addresses you can sometimes put a name to, and the data turns up at least one clearly. Wintermute – one of the largest crypto market-makers globally – is the second-largest stablecoin trader on both Solana and EVM chains, ranking behind only one anonymous address on each. Its EVM trading alone tops $13B a month. This is not a peripheral actor; it is a named, regulated-adjacent professional firm, traceable on-chain even though it operates through intermediaries. Cross-chain bridges surface too: Relay.link moved more than $1B across 65 venues rebalancing its inventory, alongside deBridge.

Machines are always on and make up most of the volume. They come in three forms.

Arbitrage bots trade thousands to millions of times a month, a few hundred dollars at a clip, across a dozen venues, every day – keeping prices aligned across platforms and extracting small price differences between them.

Aggregators – Jupiter on Solana; 1inch, 0x, CoW, and KyberSwap on EVM – take one user’s order and split it across many pools to find the best price. A single intended trade becomes several on-chain swaps. Both arbitrage bots and aggregators have been part of the DEX landscape for years.

Proprietary AMMs (automated market-makers run from private capital, with no public interface) are newly dominant. HumidiFi, SolFi, and BisonFi are the leading examples. Each quotes prices on-chain and connects directly to aggregators. Orders reach them only when an aggregator routes them there, without the trader ever choosing them. The model is not brand new; Lifinity ran one back in 2022. But the wave that now moves much of Solana’s volume is barely a year old, and it is a Solana story: only there is on-chain compute cheap enough to re-quote prices many times a second.

The behavioral signatures are unmistakable. Machines run 26-28 days a month across six to 14 venues; individuals show up two or three days on one or two. The machine-pattern addresses are a fraction of a percent of all wallets, yet they account for the large majority of volume, while the human-pattern wallets – the overwhelming majority of addresses – account for under a tenth of it.

Source: Crystal Intelligence and Dune Analytics

Source: Crystal Intelligence and Dune Analytics

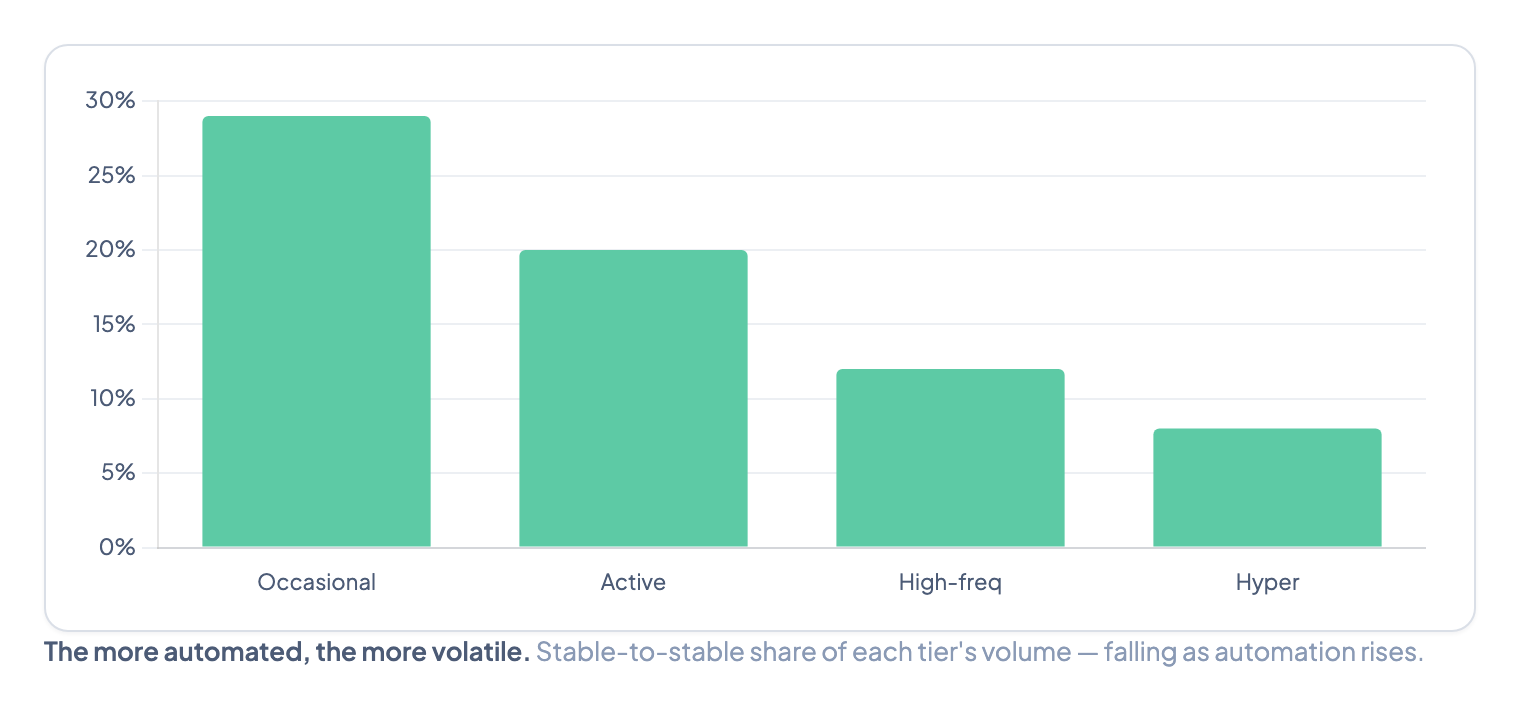

The “speculation” is the machines

As an address gets more automated, it trades less against other dollars and more against volatile assets. EVM’s busiest bots run about 90% of their volume against volatile tokens; ordinary wallets sit near 30% dollar-for-dollar. So the volatile-paired trading – the part that looks like speculation – is overwhelmingly automated arbitrage and market-making, not people taking bets. The humans, proportionally, are the ones converting between dollars.

Source: Crystal Foresight

Source: Crystal Foresight

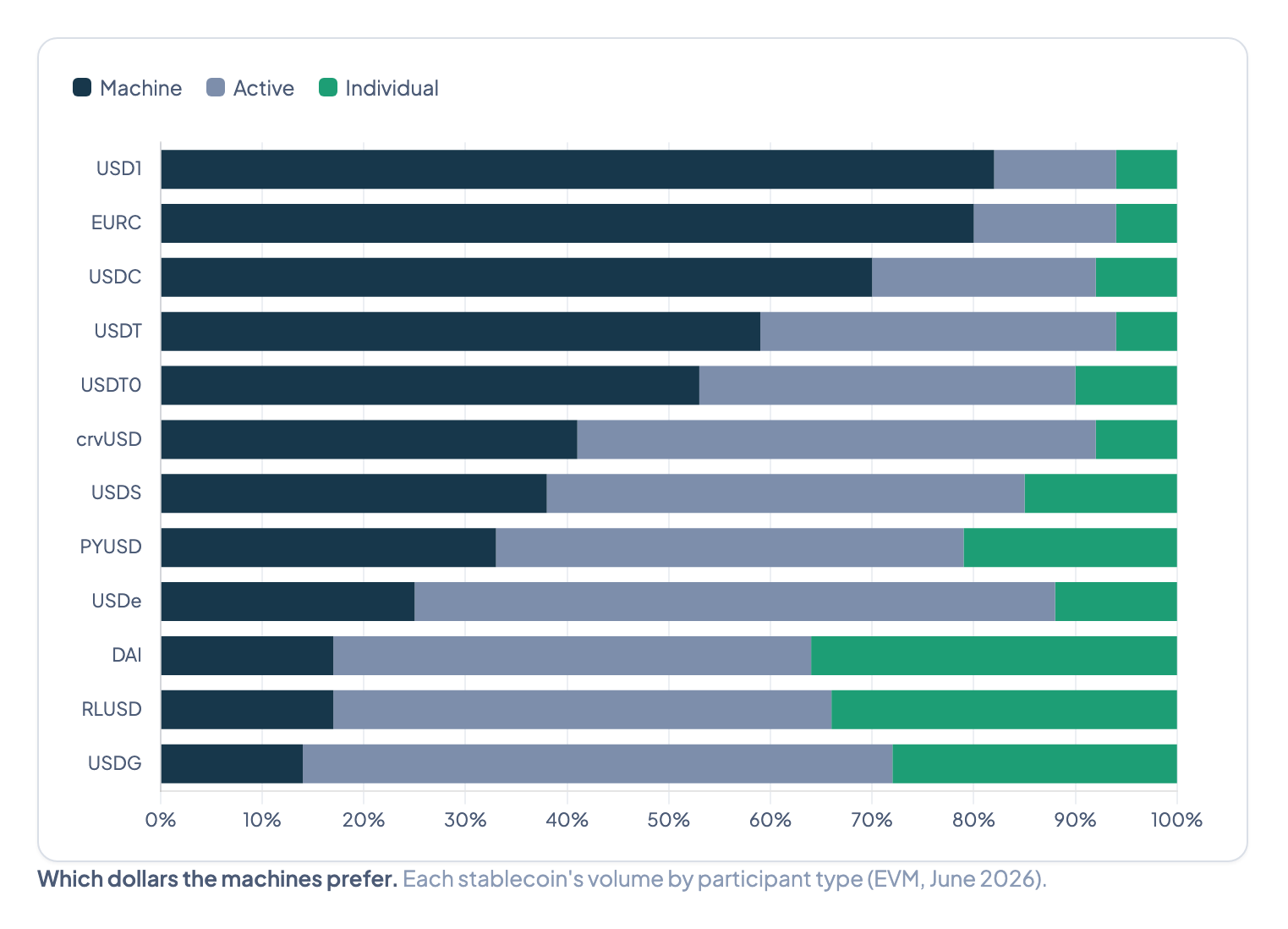

Which dollars the machines prefer

The participant mix is not the same for every stablecoin – and it is one of the more revealing things on the chain, because it separates coins whose trading reflects organic demand from coins whose volume is largely driven by automation.

The two majors are machine-heavy, as you would expect: about 70% of USDC volume and 59% of USDT volume comes from automated addresses. But the newer dollars split sharply. World Liberty’s USD1 is the most automated of all – roughly 82% of its volume is machines – which is worth noting whenever its growth is cited as adoption; most of it is bots, not buyers. Circle’s euro coin EURC is similar at about 80%, the signature of euro-dollar arbitrage rather than people spending euros.

At the other end sit the coins with a real human footprint. Ripple’s RLUSD and the decentralized dollar DAI are the most retail of the set – roughly a third of each coin’s volume comes from individual-scale wallets, and only about 17% from machines. Ethena’s USDe is different again: it is dominated by the active middle tier – yield farmers (users depositing assets into automated protocols to earn returns) and active traders entering positions – rather than by bots or by casual holders.

So when a new stablecoin posts a big volume number, the question to ask is not how large but who – and the chain answers it.

Source: Crystal Intelligence and Dune Analytics

Source: Crystal Intelligence and Dune Analytics

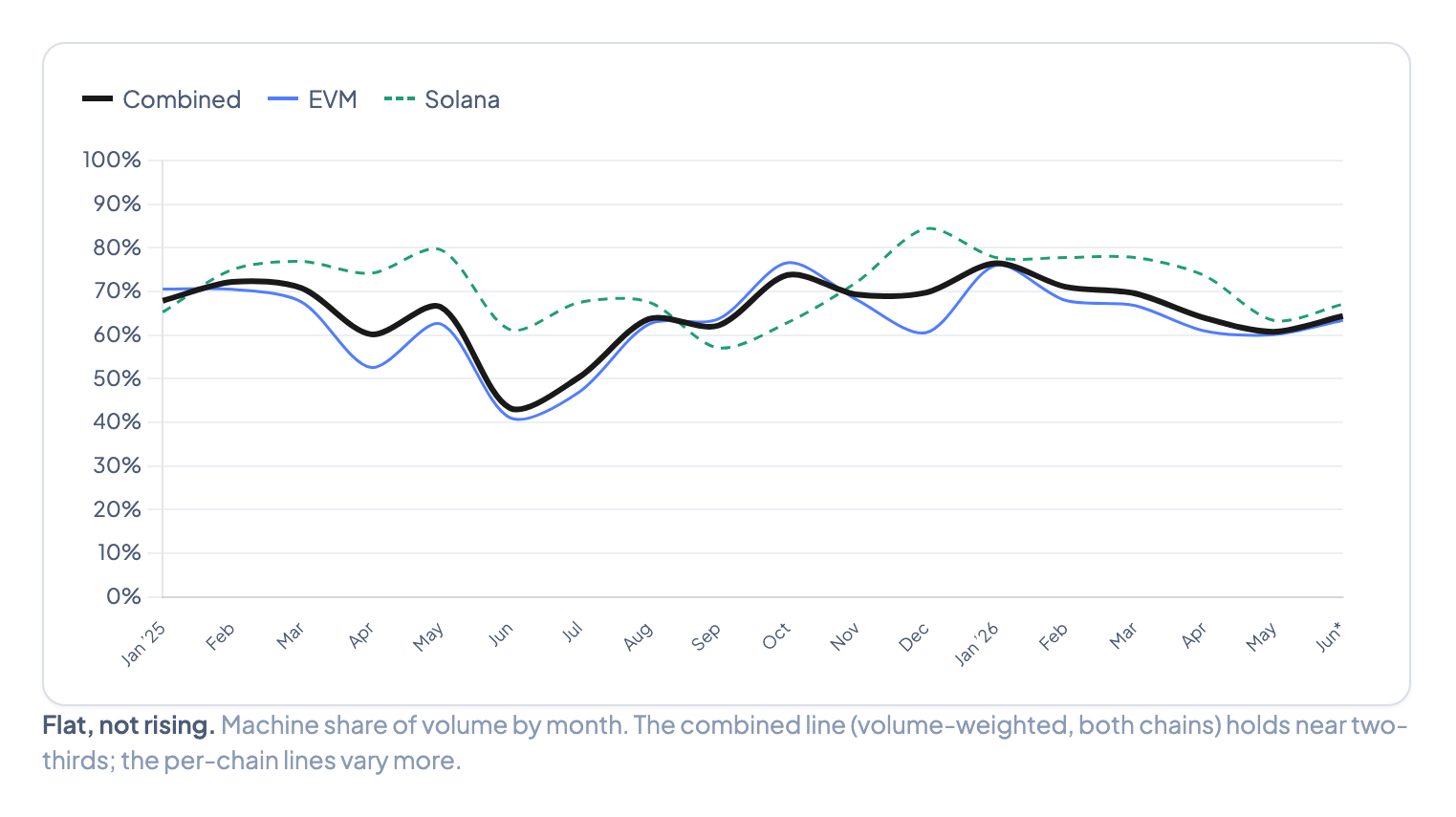

The machines were always here

It is tempting to assume machines have grown more dominant since the start of 2025 – but the data shows almost nothing moved. Across 18 months the automated share of volume has averaged about 65% and barely strayed. What movement there is runs countercyclical: the share dipped to about 43% in June 2025, when a wave of retail trading and rising prices briefly flooded the market, before climbing back as the wave receded. Machine dominance is not new, and it is not growing; it is simply constant.

This matters for how volume figures are read. If two-thirds of stablecoin DEX volume has been automated for 18 months regardless of market conditions, then rising volume is not evidence of growing human adoption. It is evidence of more machines, moving more dollars, for their own reasons.

Source: Crystal Intelligence and Dune Analytics

What actually changed: smaller, faster, invisible

The machine share held steady, but the machine layer was rebuilt underneath it. Three things moved.

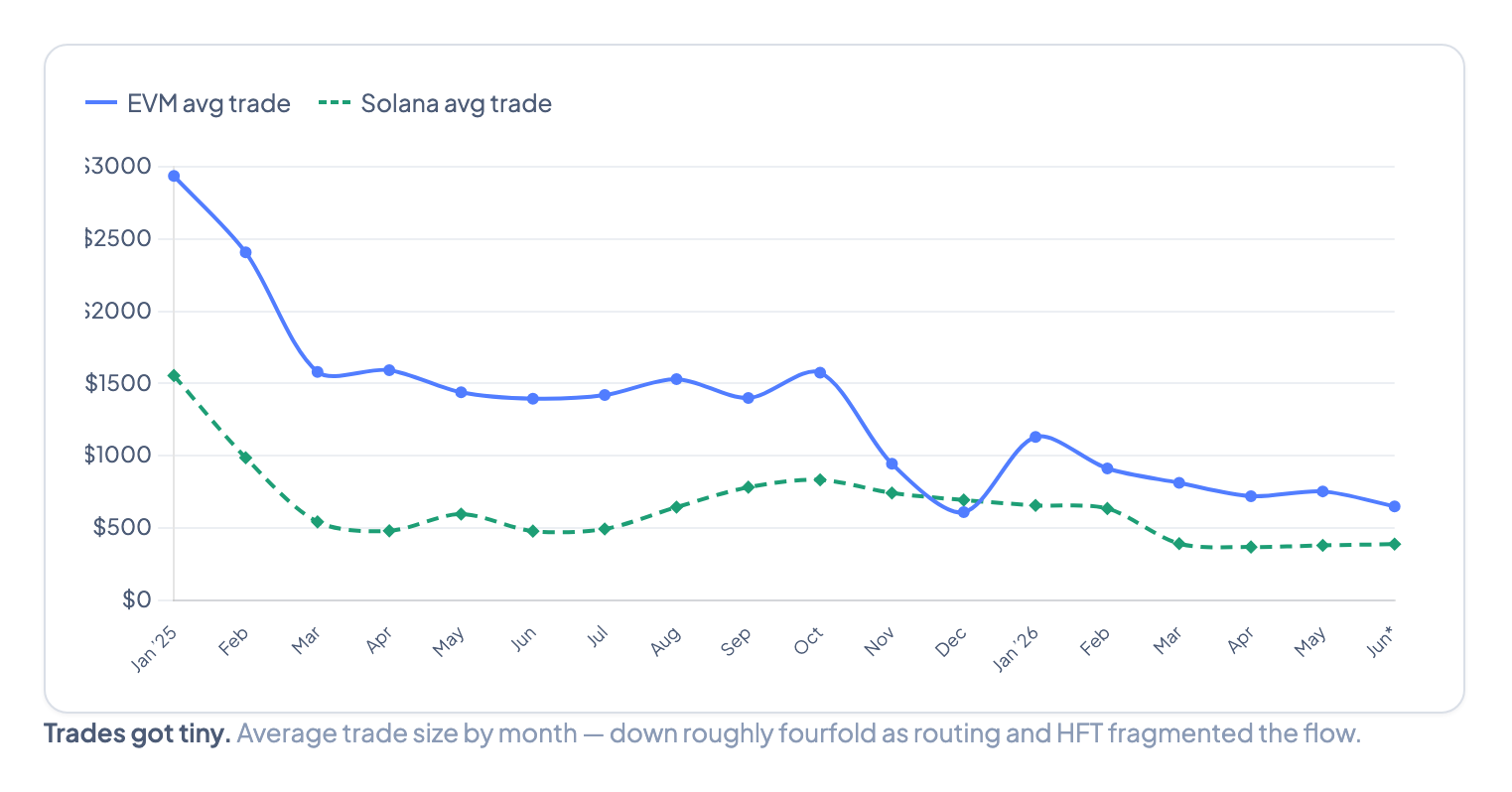

Trades got tiny. Average stablecoin trade size collapsed from about $2,940 to $700 on EVM, and from $1,550 to $380 on Solana, even as the number of trades held up. In June alone there were roughly 300 million stablecoin trades under $1,000 – about 185 million on EVM chains and 113 million on Solana. Aggregators show the texture plainly: 0x’s API alone routed more than two million trades at a median size around $10.

Source: Crystal Foresight

Source: Crystal Foresight

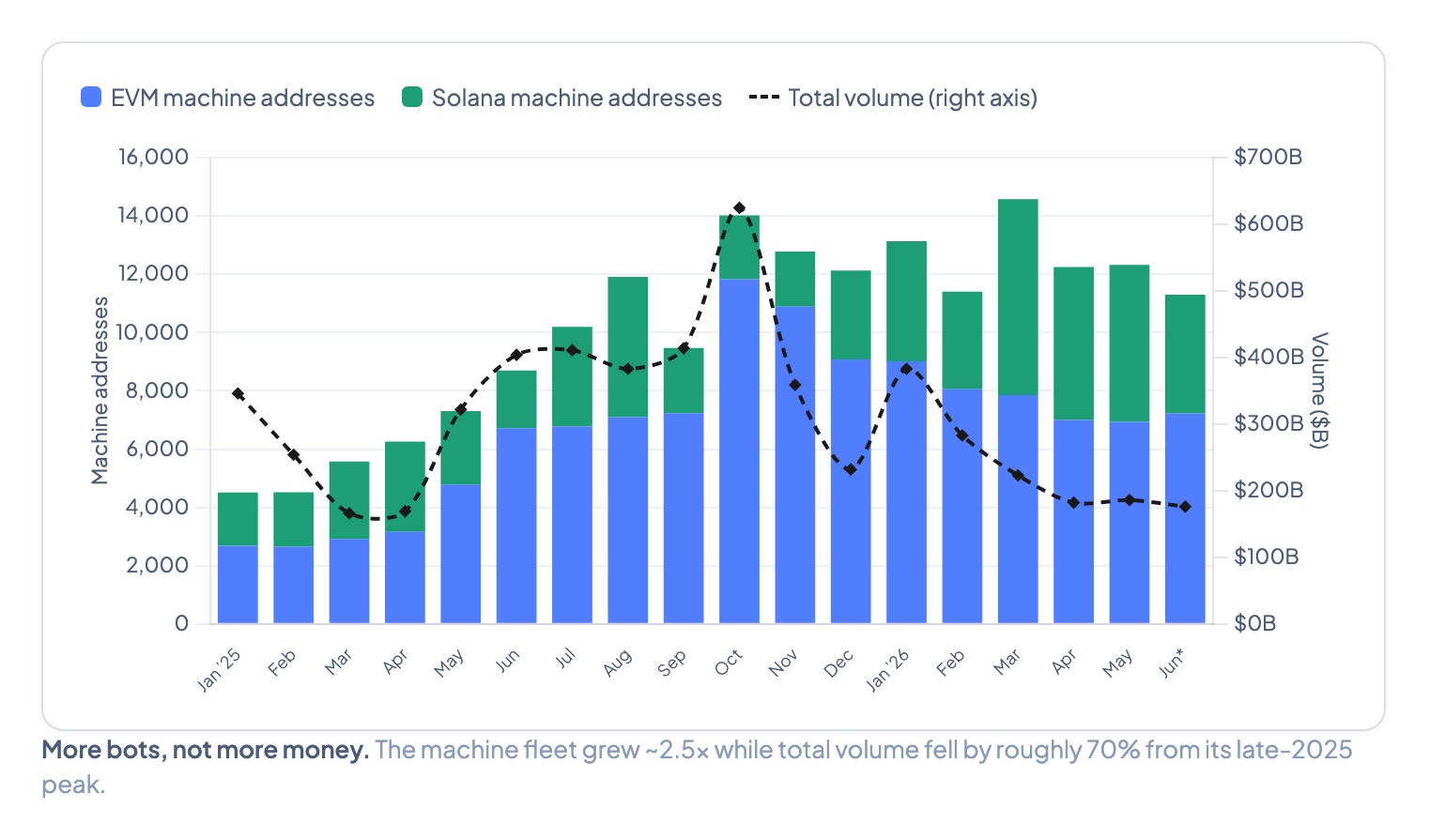

The fleet grew. The number of EVM addresses trading more than 2,000 times a month went from about 2,700 in early 2025 to a peak near 12,000, settling around 7,200. More machines, trading more often, in smaller pieces.

Source: Crystal Foresight

Source: Crystal Foresight

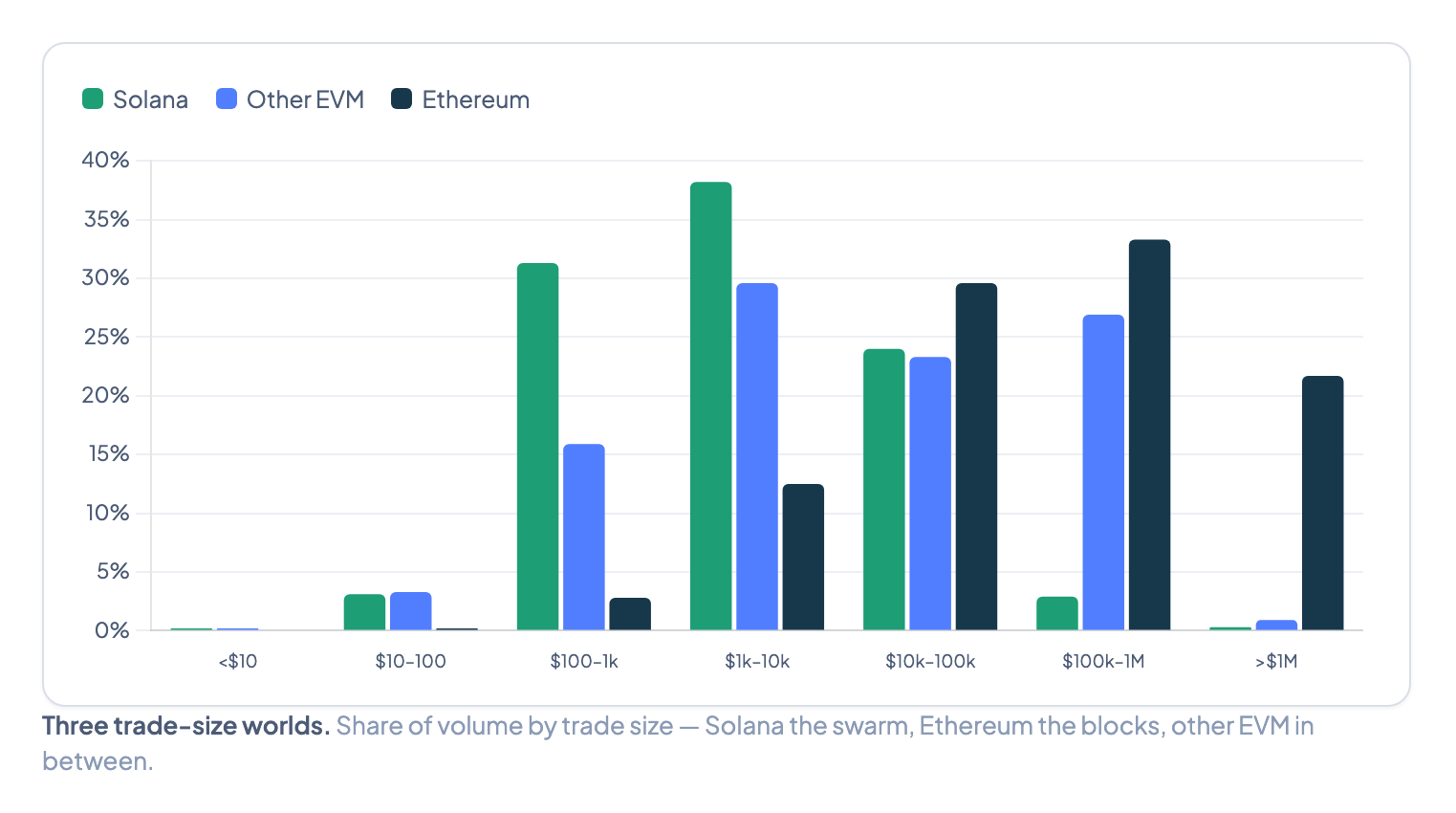

The venues went dark. Public automated market-makers – Uniswap, PancakeSwap, Raydium – still carry about 72% of volume, with StableSwap pools (a pool design optimised for stablecoin-to-stablecoin trading, led by Curve) doing roughly a tenth of that. But the fastest-growing archetype, now around 18% of all volume and almost entirely on Solana, is the proprietary AMM: no public interface, no public liquidity, reachable only through an aggregator. HumidiFi reached roughly a third of all Solana DEX volume within months of launching.

The chains express this differently. Solana is a swarm – almost everything is small and aggregator-routed, even retail orders (more than 90% of them). Ethereum is the opposite: trades above $100,000 are under 1% of its trades but about 56% of its volume; institutional participants and market-makers settle there. The other EVM chains sit in between. Ethereum, tellingly, is the outlier.

Source: Crystal Foresight

Follow the money, and some of it leaves

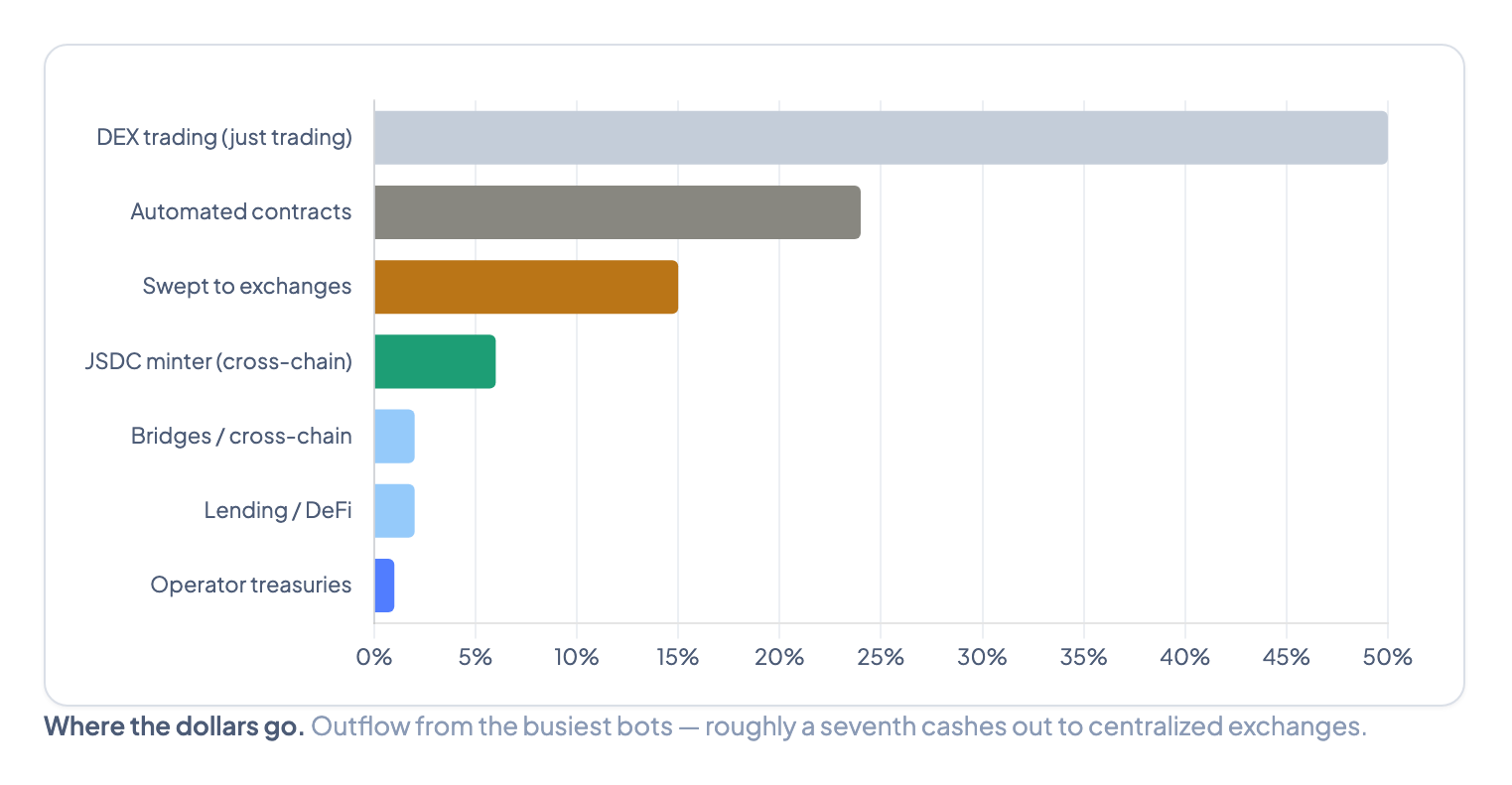

A natural question about all this machine activity: when the bots move dollars, does anything flow out beyond the trade, or does it all circulate inside the system? We traced where the busiest bots send their tokens.

About half of the outflow is simply them trading: dollars into DEX pools and routers. Another quarter goes to more automated contracts – unindexed routers and bots, the same infrastructure one layer down. About $0.15 of every dollar exits to named exchange deposit addresses – Coinbase, Binance, OKX, and Bybit. Put another way: about 75 cents of every bot dollar circulates within the on-chain system, and about 15 cents exits to named exchanges. The remaining onchain flow is the USDC minter contract, where bots burn and re-mint to move dollars between chains, plus bridges, lending, and a thin residual of market-maker treasuries.

Source: Crystal Foresight

So the bot economy is not entirely self-contained. Most of the activity stays internal – trading, rebalancing among the machines themselves – but a real and traceable slice ends up deposited at the big exchanges.

What it means

A decentralized exchange is a public ledger of who did what. Read carefully, it tells you something the volume number alone never will: most “stablecoin trading” is not trading in the sense you picture. It is a few thousand automated systems – arbitrage bots, aggregator routers, and market-makers – moving dollars between each other and across volatile markets, with a long tail of people doing comparatively little.

For compliance teams and institutional participants, this changes how DEX volume should be interpreted. A rising volume figure does not mean more people are using stablecoins; it may mean more bots, running more strategies, through infrastructure that has no public face. For investigators, the same ledger that reveals machine dominance also names the players: Wintermute’s $13B monthly EVM footprint is traceable, and the flow from bot wallets to Coinbase, Binance, and OKX deposit addresses is on-chain and auditable.

The chain does not show everything. It does not tell you who owns the bot or why they are trading. But it is the only place where the question of who is actually behind stablecoin volume has any answer at all.

Frequently asked questions

Is “machine” trading bad?

No. Arbitrage and market-making keep prices consistent across venues and tighten spreads for everyone – that is useful work. The point is not that automation is wrong; it is that a single volume figure hides who is doing the trading and why, which matters if you are reading that figure as a sign of human adoption.

Does “mostly machines” mean it isn’t real people?

“Bot” describes the method, not the operator: a wallet trading thousands of times a day is automated, but the operator could be a major market-maker or one person running a strategy from a laptop. The data shows the activity is overwhelmingly automated and cycles through shared infrastructure; it does not tell you who owns the operation behind each bot.

How can you tell a bot from a person without names?

By behavior. A wallet that trades 28 days a month, across a dozen venues, thousands of times, at a few hundred dollars a trade, is not a person. One that appears twice a month on a single venue probably is. We classify by these signatures – trade count, active days, venue spread, trade size – and are candid that it is a classification method, not a definitive census.

What is a “proprietary AMM,” and why does it have no website?

It is a market-maker that quotes prices on-chain from its own capital and connects directly to aggregators. Users never interact with it; the aggregator routes orders to whichever venue offers the best price. No storefront is needed. HumidiFi, SolFi, and BisonFi are examples – among the largest venues on Solana, with no public interface.

If volume is down, how is activity up?

Dollar volume fell by about 70% from its late-2025 peak, but the number of trades did not. Trades simply got much smaller – average sizes fell roughly fourfold – as aggregator routing and high-frequency strategies fragmented the same flow into far more, far tinier pieces.

Do the newer stablecoins behave differently from each other?

Strikingly so – see “Which dollars the machines prefer” above. They also differ in what they trade against: most newer stablecoins trade almost entirely against other dollars (cycling in and out of yield and borrowing positions), where the two majors trade heavily against volatile assets. That asset-pair breakdown is a companion analysis to this one.

Data as of 25 June 2026. Figures derived from Crystal Intelligence and Dune Analytics on-chain data. DEX volume is gross and includes automated and aggregator-routed activity; figures are directional. June 2026 is a partial month to the 25th. This report is for informational purposes only and does not constitute investment advice.